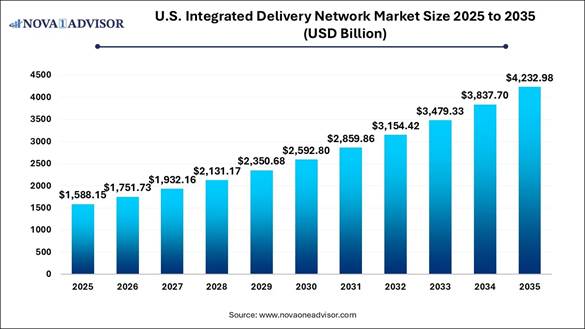

According to Nova One Advisor, the U.S. integrated delivery network market size was valued at USD 1,588.15 billion in 2025 and is poised to grow from USD 1,751.73 billion in 2026 to USD 4,232.98 billion by 2035, at a CAGR of 10.3% during the forecast period 2026-2035.

Key Takeaways

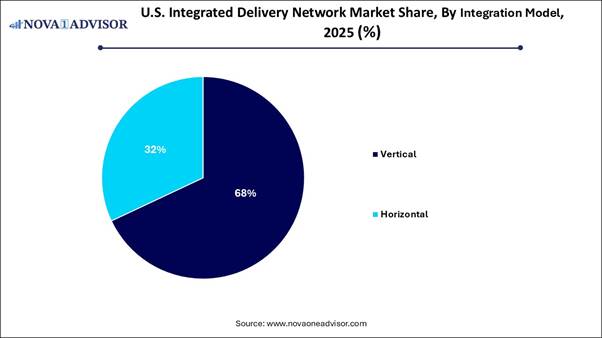

⬥︎ By integration model, the vertical segment generated the biggest market share in 2025.

⬥︎ By integration model, the horizontal segment is expanding at the fastest CAGR between 2026 and 2035.

⬥︎ By service type, the acute care segment accounted for the largest market share in 2025.

⬥︎ By service type, the primary care segment is projected to grow at a solid CAGR between 2026 and 2035.

The Complete Study is Now Available for Immediate Access | Download the Sample Pages of this Report@ https://www.novaoneadvisor.com/report/sample/8206

Undergoing a high-stakes, technology-driven transformation, the healthcare sector is shifting from traditional care models to a unified, value-based system that vertically integrates inpatient, ambulatory, and specialty services, which is driving market growth. As regional giants emerge, the race for operational efficiency is accelerating the move toward AI-driven workflows, including generative AI, ambient documentation, and advanced interoperability. These advances aim to reduce administrative leakage, control chronic care costs, and alleviate staff burnout across the entire care continuum.

Market Overview: The Future of Integrated Care

The U.S. integrated delivery network market is a powerhouse that is rapidly evolving toward unified, technology-enabled, and vertically integrated healthcare systems. This transformation is reshaping American healthcare by aligning hospitals, clinics, and digital systems. Factors such as an aging population, increasing chronic care demands, and the urgent shift to value-based, outcome-driven reimbursement are motivating vertically and horizontally integrated organizations to invest heavily in IT. Key players like HCA Healthcare, Mayo Clinic, and Kaiser Permanente are optimizing efficiency to provide high-quality, cost-effective care.

What are the different types of IDNs?

Healthcare IDNs (Integrated Delivery Networks) can be categorized into four types, based on the number of healthcare facilities involved and the approach to strategic decisions such as purchasing and care coordination. These IDNs fall under one of the following integration levels:

· System II (Horizontal Integration): Typically, these are regional or national multi-hospital networks. System II networks primarily focus on owning and managing hospitals, although they may also include other care facilities. Many government, state, or investor-owned IDNs fall under this category.

· System III (Vertical Integration): These networks offer comprehensive healthcare services that span the entire continuum of care. They include a wide range of facilities within the same system, from prenatal care to assisted living and hospice services. The goal of a vertically integrated health system is to promote shared information and resources across all facilities. Many academic, Catholic, and community-based health systems are considered System III networks.

· System IV (Strategic Integration): These are advanced vertically integrated networks that exhibit a high level of strategic coordination and organization. System IV networks align information systems, centralized administrative control, purchasing, and distribution processes across all facilities within the network, ensuring efficiency and consistency.

Why are integrated delivery networks important in healthcare?

Much like accountable care organizations (ACOs), IDNs use their vast networks of healthcare providers to deliver high-quality, coordinated care to patients. Because of the wide range of care services IDNs can offer, they can address nearly all of their patients’ needs without seeking out-of-network referrals. This not only allows for greater communication and care collaboration across a patient’s whole continuum of care but also helps to prevent revenue loss from network leakage.

Some large integrated delivery networks are also able to leverage their market influence for greater negotiating power in the same way a group purchasing organization (GPO) would. This allows IDNs to secure competitive supply chain prices which in turn can help lower overall healthcare costs.

You can place an order or ask any questions, please feel free to contact at sales@novaoneadvisor.com | +1 804 441 9344

U.S. Integrated Delivery Network Market Report Scope

|

Report Attribute |

Details |

|

Market Size in 2026 |

USD 1,751.73 Billion |

|

Market Size by 2035 |

USD 4,232.98 Billion |

|

Growth Rate From 2026 to 2035 |

CAGR of 10.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2035 |

|

Segments Covered |

Integration Model, Service Type |

|

Market Analysis (Terms Used) |

Value (US$ Million/Billion) or (Volume/Units) |

|

Report Coverage |

Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

|

Key Companies Profiled |

HCA Healthcare; Ascension; Kaiser Foundation Health Plan, Inc.; UNITEDHEALTH GROUP; Providence; UPMC; Trinity Health; TH Medical; CHSPSC, LLC; CommonSpirit Health |

Buy Now Full Report: https://www.novaoneadvisor.com/report/checkout/8206

Healthcare’s Evolution from Reactive to

Predictive: Major Potential Integrated delivery networks have a

significant opportunity to transition from reactive to predictive,

personalized, and proactive care. By leveraging AI-driven digital

transformation and integrating electronic

health records (EHRs) and remote monitoring, they can enhance care

coordination. Utilizing machine

learning for real-time risk assessments, such as predicting sepsis, can

substantially reduce hospital readmissions, optimize resource allocation, and

improve care quality. This digital maturation allows for personalized

treatments and better patient outcomes through proactive, targeted

interventions. High Capital Expenditure and Supply

Chain Volatility: Major Limitation U.S. integrated delivery networks face

substantial growth constraints due to high capital requirements for

technological upgrades (such as AI and cloud systems) and rising supply chain

costs, exacerbated by equipment tariffs. This financial pressure hampers

immediate expansion and consolidation efforts, serving as a critical barrier to

rapid infrastructure innovation and operational efficiency. U.S. Integrated Delivery Network Market:

State Analysis California: Vertical Integration Leader

California focuses on combining

payer-provider models (insurers and hospitals) with advanced EHR

interoperability to manage total care costs. Key players include Kaiser

Permanente, Dignity Health, and Prime Healthcare, all of which prioritize

seamless digital patient experiences. Texas: Expansion and Volume Hub Texas experiences rapid growth in

horizontal networks driven by population influx and a high rate of mergers and

acquisitions of independent hospitals. Major entities like Baylor Scott &

White, Tenet Healthcare, and HCA Houston Healthcare are focused on increasing

market share. New York: Value-Based Care Adoption New York emphasizes high-acuity care,

integrated post-acute care, and regional care coordination, influenced by

strict regulatory environments and a strong focus on quality metrics. Leaders

include Northwell Health, New York-Presbyterian, and Mount Sinai. Florida: Consolidation and Senior Care Florida has a high density of integrated

delivery networks concentrating on Medicare Advantage, chronic care management,

and services for an aging population due to demographic factors. Key players

include Advent Health and Baptist Health South Florida, which are optimizing

care for chronic conditions. Tennessee: Operations and Technical

Support Tennessee serves as a major hub for

national for-profit integrated delivery networks focused on operational

efficiency, staffing, and supply chain management. Major players include HCA

Healthcare and Community Health Systems, which emphasize high-volume,

cost-efficient care. Immediate Delivery is Available | Get

Full Report Access@ https://www.novaoneadvisor.com/report/checkout/8206

U.S. Integrated Delivery Network Market:

Segmentation Analysis By Integration Model Analysis The vertical segment dominated the market

in 2025. This dominance was achieved by strategically aligning payers,

hospitals, physicians, and post-acute care under one entity to manage the

entire care continuum. These integrated networks oversee patient care from

primary diagnosis to inpatient treatment and post-acute rehabilitation,

allowing them to manage care quality and costs throughout the entire patient

journey. The shift from volume-driven to value-based payment models is driving

this adoption, as vertically integrated entities can reduce costs, optimize

patient outcomes, and gain a competitive advantage in health management. The horizontal segment is expected to

experience the fastest growth during the forecast period. This growth is mainly

driven by widespread hospital mergers and acquisitions, which aim to expand

regional footprints, leverage economies of scale, and manage healthcare costs.

Horizontal models contribute to reduced costs and increased operational

efficiency by streamlining management across multiple locations and

strengthening negotiation positions with insurers. This strategy allows providers

to consolidate suburban and urban markets, establishing comprehensive, uniform

service levels across a larger territory. By Service Type Analysis The acute care segment led the market in

2025, primarily due to the provision of comprehensive, high-acuity services

such as surgeries, emergency care, and intensive care units (ICUs) within a

single network. This focus on efficient, value-based care leads to better

patient outcomes. Advanced diagnostic tools, AI-enabled clinical workflows, and

electronic health record (EHR) interoperability enhance operational efficiency

and care quality, solidifying the role of hospital settings. Acute care

facilities capitalize on their ability to provide immediate treatment for

critical conditions, yielding high-value returns within the accountable care

organization model and strengthening top-tier acute care providers. The primary care segment is expected to

grow the fastest during the forecast period. This growth is largely driven by

the shift toward value-based care, the rising prevalence of chronic diseases,

and an emphasis on preventative, cost-effective care. The transition from

volume to value incentivizes integrated delivery networks to invest in primary

care to better manage chronic diseases, reduce costs, and enhance care quality.

These networks are increasingly merging with or acquiring primary care

practices to create comprehensive care pathways, from diagnosis to ongoing

management. Primary care within an integrated delivery network helps optimize

patient flow, ensuring seamless transitions to acute or specialist care when

necessary. U.S. Integrated Delivery Network Market

Companies ·

HCA Healthcare: HCA

Healthcare operates a vast network of 190 hospitals and around 2,400 ambulatory

sites, offering a broad range of services through horizontal integration,

enhancing operational efficiency. ·

Ascension: Ascension

is a large, faith-based non-profit health system that provides comprehensive

care across multiple states, with a focus on serving vulnerable populations.

·

Kaiser Foundation Health Plan, Inc. (Kaiser

Permanente): Kaiser Permanente exemplifies a

vertically integrated healthcare model, combining its health insurance plans,

hospitals, and physician groups under one unified organization. ·

UnitedHealth Group: UnitedHealth Group plays a major role through its two complementary

divisions: UnitedHealthcare (health benefits) and Optum (technology-driven

health services, including direct care and pharmacy benefits). ·

Providence: Providence

is a significant not-for-profit health system that offers a broad spectrum of

services across multiple states, with an emphasis on community health and

social justice initiatives. ·

UPMC (University of Pittsburgh Medical

Center): UPMC operates as an integrated

"payvider" system, blending a health insurance division with an

extensive network of hospitals and physician practices. ·

Trinity Health: Trinity

Health is a large Catholic non-profit health system, serving communities with

high-quality, sustainable healthcare across many regions. ·

TH Medical: TH

Medical is likely a subsidiary or division within the larger Trinity Health

network, contributing to specific operational aspects. ·

CHSPSC, LLC: CHSPSC,

LLC is the management and consulting division of Community Health Systems, Inc.

(CHS), overseeing a large network of hospitals and clinics throughout the U.S.

·

CommonSpirit Health: CommonSpirit Health is one of the largest non-profit health systems

in the U.S., operating a wide array of hospitals and care sites across 23

states. Key Initiatives for the U.S. Integrated

Delivery Network Market State Initiative and Program Focus and Impact California CalAIM (California Advancing and Innovating Medi-Cal) A multi-year initiative driving integrated delivery networks to

adopt population health management, offering enhanced care management and

community supports to integrate physical, behavioral, and social services. New York NY Delivery System Reform Incentive Payment (DSRIP) Evolution Focuses on sustaining integrated delivery network collaboration

and regional health information exchange (HIE) to transition toward

value-based payment (VBP) models, emphasizing public-private partnerships. Massachusetts Health Equity and Quality Improvement Program State-driven mandates require large integrated delivery networks

to report on equity metrics and invest in community-level health initiatives,

fostering vertical integration with local entities. Pennsylvania Rural Health Model and Digital Innovation Focus Supports integrated delivery networks in improving care

coordination across rural-urban settings through telehealth and sustainable

payment models to reduce hospital readmissions. North Carolina Healthy Opportunities Pilots (Medicaid Innovation) A first-of-its-kind initiative where integrated delivery networks

like Advocate Health/Atrium are reimbursed for addressing non-medical drivers

of health to lower total cost of care.

Major Shifts in the U.S. Integrated

Delivery Network Market ·

In February 2026, JD.com announced JoyExpress,

its dedicated express delivery service in Europe, as part of JINGDONG

Logistics. JoyExpress will support Joybuy, providing same-day and next-day

delivery in major cities, with teams based in the UK, Germany, the Netherlands,

and France. The service includes integrated delivery and installation for large

home appliances, emphasizing professionalism with branded uniforms and

vehicles, aiming to expand as Joybuy grows. ·

In October 2025, JoyLogistics launched an

integrated delivery and installation service for bulky items in Malaysia and

Singapore, offering next-day delivery in Kuala Lumpur. This service provides

end-to-end support, including in-home setup and seamless returns. JoyLogistics

utilizes its global logistics network, operating nine overseas warehouses in

Southeast Asia for efficient same-day and next-day delivery. ·

In March 2025, the Cleveland Clinic partnered

with G42 to leverage AI for enhancing patient care and optimizing healthcare

operations. The collaboration aims to create a task force focused on AI-powered

advancements, with G42 specializing in AI and big data analytics. Cleveland

Clinic’s CEO, Tom Mihaljevic, highlighted the potential of AI to improve

patient care and outcomes, while G42’s CEO, Peng Xiao, emphasized the

transformative opportunities AI brings to the healthcare industry. Related Report – ⬥︎ Viral Capsid Development Market - https://www.novaoneadvisor.com/report/viral-capsid-development-market

⬥︎ Cell Therapy Human Raw Materials Market - https://www.novaoneadvisor.com/report/cell-therapy-human-raw-materials-market

⬥︎ Scaffold-free 3D Cell Culture Market - https://www.novaoneadvisor.com/report/scaffold-free-3d-cell-culture-market

⬥︎ Effective Microorganisms Market - https://www.novaoneadvisor.com/report/effective-microorganisms-market

⬥︎ Automated Liquid Handling Technologies Market - https://www.novaoneadvisor.com/report/automated-liquid-handling-technologies-market

⬥︎ Platelet Rich Plasma Market - https://www.novaoneadvisor.com/report/platelet-rich-plasma-market

⬥︎ Synthetic Gene Circuits Market - https://www.novaoneadvisor.com/report/synthetic-gene-circuits-market

⬥︎ Lyophilization Equipment And Services Market - https://www.novaoneadvisor.com/report/lyophilization-equipment-and-services-market

⬥︎ Cell Culture Media & Cell Lines Market - https://www.novaoneadvisor.com/report/cell-culture-media-cell-lines-market

⬥︎ Automated Cell Counting Market- https://www.novaoneadvisor.com/report/automated-cell-counting-market

⬥︎ Primary Cell Culture Market - https://www.novaoneadvisor.com/report/primary-cell-culture-market ⬥︎ Fetal Bovine Serum Market - https://www.novaoneadvisor.com/report/fetal-bovine-serum-market

U.S. Integrated Delivery Network Market

Report Segmentation This report forecasts revenue growth at

country levels and provides an analysis of the latest industry trends in each

of the sub-segments from 2021 to 2035. For this study, Nova one advisor, Inc.

has segmented the U.S. Integrated Delivery Network market. By Integration Model ·

Vertical ·

Horizontal By Service Type ·

Acute Care ·

Primary Care ·

Long-term Health ·

Specialty Clinics ·

Other Services Immediate Delivery

Available | Buy This Premium Research https://www.novaoneadvisor.com/report/checkout/8206 About-Us Nova One Advisor is a global leader

in market intelligence and strategic consulting, committed to delivering deep,

data-driven insights that power innovation and transformation across

industries. With a sharp focus on the evolving landscape of life sciences, we

specialize in navigating the complexities of cell and gene therapy, drug

development, and the oncology market, enabling our clients to lead in some of

the most revolutionary and high-impact areas of healthcare. Our expertise spans the entire

biotech and pharmaceutical value chain, empowering startups, global

enterprises, investors, and research institutions that are pioneering the next

generation of therapies in regenerative medicine, oncology, and precision

medicine. Web: https://www.novaoneadvisor.com/ Our Trusted Data Partners: Nova One Advisor - Market

Research Reports & Consulting Firm Nova One Advisor offers

comprehensive market research reports with in-depth industry analysis and

market data. Call us: +1 804 420 9370 Email: sales@novaoneadvisor.com Web: https://www.novaoneadvisor.com/ You can place an order or ask any

questions, please feel free to contact at sales@novaoneadvisor.com | +1 804 441 9344