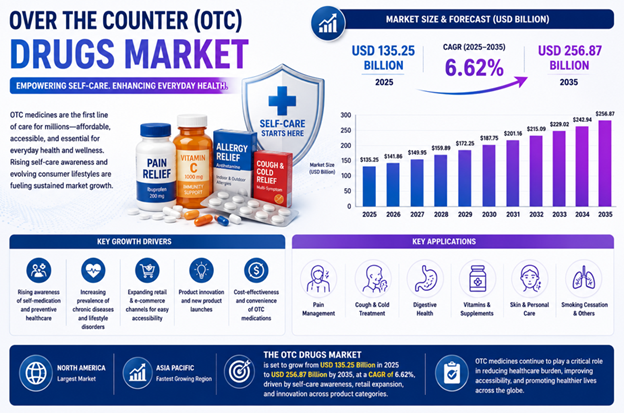

The global over-the-counter (OTC) drugs market is undergoing a remarkable transformation, driven by the convergence of digital technology, consumer wellness trends, and regulatory evolution. With a market size of USD 135.25 billion in 2025, projected to reach USD 256.87 billion by 2035 at a CAGR of 6.62%, OTC medications are becoming a strategic cornerstone of proactive self-care and accessible healthcare solutions.

From pharmacy shelves to personalized wellness, the over-the-counter (OTC) drugs market is undergoing a significant digital transformation. It is shifting from traditional symptom relief methods to an intelligent, personalized, and proactive consumer health ecosystem. This change is driven by AI-powered self-selection tools, e-commerce personalization, and blockchain-verified supply chains. As a result, consumers can now make self-care decisions in minutes instead of days, turning the convenience of quick fixes into a reliable and high-precision approach to personal wellness management.

Where Data Meets Strategic Clarity 📥 View Sample Pages of the Complete Report 👉 https://www.precedenceresearch.com/sample/1466

Over the Counter (OTC) Drugs Market Key Takeaways

🔹North America dominated with the largest market share in 2025.

🔹Europe is expected to have the fastest growth with a notable CAGR during the forecast period.

🔹By product, the cough and cold products segment contributed the highest market share in 2025.

🔹By product, the analgesics segment is growing at a strong CAGR between 2026 and 2035.

🔹By route of administration, the oral segment captured the highest market share of 56.66% in 2025.

🔹By route of administration, the parenteral segment is poised to grow at a healthy CAGR between 2026 and 2035.

🔹By distribution channel, the drug stores and retail pharmacies segment generated the biggest market share in 2025.

🔹By distribution channel, the online pharmacies segment is expanding at the fastest CAGR between 2026 and 2035.

Market Overview: The Surge in Global Self-Medication

The global OTC drug market comprises non-prescription medications that consumers can select to treat minor health conditions without medical supervision. These products are commonly available in pharmacies and retail stores. A strong shift towards self-medication and a growing geriatric population are major drivers of this market. Regulator-approved medications, including analgesics, dermatology products, and vitamins, have become essential for proactive health management. Market players are focusing on innovation to meet the needs of health-conscious consumers.

🔸 Recent surveys indicate that 68% of adults prefer OTC remedies for minor ailments to avoid long wait times for physician appointments, highlighting the growing role of self-directed healthcare decisions.

➡️ Become a valued research partner with us ☎ https://www.precedenceresearch.com/schedule-meeting

AI-Driven Personalization in Pharmacy: Major Potential

The rapid move towards digital pharmacy, accelerated by AI-driven symptom checkers, telepharmacy, and intelligent self-selection tools, is unlocking significant opportunities to transition complex prescription (Rx) drugs to OTC status. By enabling safe, personalized self-medication without requiring immediate consultation with a physician, this digital revolution is greatly expanding the addressable market. It enhances consumer access to care and allows for data-driven, tailored product recommendations.

Platforms like HealthTap and GoodRx AI assist consumers in selecting appropriate OTC medications, demonstrating real-time efficacy in guiding self-care choices.

Regulatory Fragmentation and Misuse Concerns: Major Limitation

Despite its growth, the global market faces significant challenges. Regulatory fragmentation, characterized by inconsistent regulations across borders and prolonged approval processes (typically 18-36 months), hinders innovation and rapid expansion. Additionally, concerns regarding consumer misuse, overdosage, and drug interactions pose major risks that threaten brand reputation and invite regulatory scrutiny, which can impede smooth market growth.

Discover What’s Driving the Market Forward👉 https://www.precedenceresearch.com/over-the-counter-drugs-market

Over the Counter (OTC) Drugs Market Report Coverage

|

Market Scope |

Details |

|

Market Size in 2025 |

USD 135.25 Billion |

|

Market Size in 2030 |

USD 187.75 Billion |

|

Market Size in 2035 |

USD 256.87 Billion |

|

Market Growth Rate (2026-2035) |

CAGR of 6.62% |

|

Largest Regional Market |

North America |

|

Fastest Growing Region |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2035 |

|

Key Growth Driver |

Increasing self-medication trends, aging population, rising health awareness, and AI-driven digital tools for consumer health |

|

Major Technology Trend |

AI-powered symptom checkers, telepharmacy, digital self-selection tools, e-commerce personalization, and blockchain verification |

|

Key Market Opportunity |

Rx-to-OTC conversions, online pharmacy expansion, emerging markets adoption, and wellness-focused product development |

|

Major Market Challenge |

Regulatory fragmentation, risk of misuse, overdosage, and inconsistent approval processes across regions |

|

Segments Covered |

By Product, By Route of Administration, By Distribution Channel, By Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

|

Key Companies Profiled |

Bayer AG, Takeda Pharmaceutical Company Ltd., Pfizer, Johnson & Johnson Services Inc., Sanofi S.A., Reckitt Benckiser Group PLC, Novartis AG, Boehringer Ingelheim International GmbH, GlaxoSmithKline PLC, Mylan |

Built for leaders who move markets. Access live, actionable intelligence with Precedence Q. https://www.precedenceresearch.com/precedenceq/

Over-the-Counter (OTC) Drugs Market: Regional Analysis

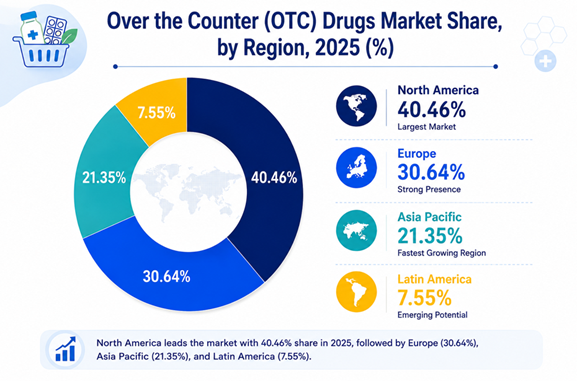

North America is expected to dominate the market by 2025, primarily due to high consumer adoption of self-medication, a strong retail pharmacy infrastructure, and a rapid transition from prescription to OTC products. The widespread retail pharmacy network, along with easy access to information about OTC drugs, facilitates frequent purchases. Favorable regulatory frameworks, particularly from the U.S. FDA, support the swift transition of drugs from prescription to OTC status, increasing product availability and consumer access.

The U.S. benefits from a strong self-care culture, an aging population, and a significant number of Rx-to-OTC switches encouraged by the FDA and driving the global market. There is a growing demand for both branded and natural products, leading to rapid evolution in this sector. Retail pharmacies are capturing the major market, while online sales are experiencing substantial growth.

🔸 In December 2025, the FDA’s new ACNU rule streamlined the process for transitioning chronic condition medications, such as statins, from prescription to OTC status by utilizing digital self-selection tools. This regulatory change aims to enhance patient access to preventative therapies without the need for a doctor's visit. (Source: FDA Gov)

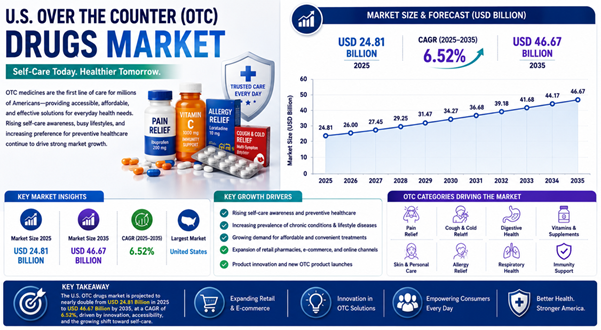

What is the U.S. Over the Counter (OTC) Drugs Market Size and Growth Rate?

The U.S. over the counter (OTC) drugs market size stood at USD 24.81 billion in 2025 and is projected to be worth around USD 46.67 billion by 2035, expanding at a CAGR of 6.52% from 2026 to 2035.

The AI in Life Sciences Market Report is Readily Available 📥 Download Sample Pages of the Report 👉 https://www.precedenceresearch.com/sample/3753

Canada is also emerging as a notable player in the region. Factors contributing to this growth include long wait times for doctors and a public health system that encourages self-care for non-urgent ailments. Health-conscious consumers are increasingly turning to natural remedies, and a robust pharmacy sector, alongside bilingual counseling and trusted guidance, is accelerating demand for self-medication solutions.

Europe is experiencing the fastest growth during the forecast period. This

expansion is attributed to a marked shift towards self-medication, an aging

population, and significant regulatory changes. Regulatory bodies, such as the

UK's MHRA, are expediting the transition of prescription drugs to OTC status

for conditions like allergies, migraines, and women's health, thereby

broadening the available OTC product range. With one of the world's oldest

populations, Europe sees seniors increasingly utilizing OTC drugs for chronic

but manageable conditions, such as joint pain, insomnia, and digestive issues,

promoting a self-care approach to chronic disease management.

Germany leads the European market for OTC medications, where the majority of sold medicine packages are non-prescription. This success is driven by high consumer trust in pharmacies and significant annual sales of Green Prescriptions for products like pain relievers and cough remedies. The market exhibits a balance between traditional pharmacy reliance and a growing e-commerce presence, supported by strict regulations.

🔸 In January 2025, Germany's new Medical Research Act (MFG) strengthens the pharmaceutical industry by permitting confidential reimbursement agreements. This protects companies focused on research and development from stringent international reference pricing pressures while promoting local clinical research. (Source: Pharmaceutical Technology)

France is actively promoting a pro-self-care agenda that combines traditional pharmacy expertise with an increasing emphasis on natural phytopharmaceuticals. Key players such as Sanofi, Pierre Fabre, Boiron, and Arkopharma dominate the market, benefiting from high consumer trust in pharmacists along with a rapidly growing, highly regulated online channel. This favorable environment focuses on prevention, supporting the wellness and natural health sector.

Get informed with deep-dive intelligence on AI’s market impact https://www.precedenceresearch.com/ai-precedence

Over-the-Counter (OTC) Drugs Market Segmental Analysis

By Product Analysis

The cough and cold products segment dominated the market in 2025, primarily due to the need for immediate relief from high-incidence respiratory illnesses. Consumers tend to prefer OTC remedies for quick symptom management rather than consulting healthcare providers. There is an increased focus on multi-symptom relief, alongside the popularity of consumer-friendly formats like fast-dissolving tablets, oral strips, and liquid sachets. The rise of e-commerce and the availability of these products in retail pharmacies make them readily accessible, reducing the need for prescriptions.

The analgesics segment is anticipated to experience the fastest growth in the forecast period. This is largely attributed to the rising prevalence of chronic pain, an aging population, and growing trends in self-medication. Manufacturers are introducing innovative formats that improve efficacy and convenience, driving market demand. Additionally, the increasing incidence of lifestyle-related stress, headaches, and chronic pain, particularly among younger working populations, boosts the consumption of painkillers. Consumers increasingly favor OTC solutions for minor aches and pains to avoid lengthy hospital visits.

By Route of Administration Analysis

The oral segment led the market in 2025, primarily due to the high adoption of tablets, capsules, and liquids. This trend is driven by the convenience of self-administration without medical supervision and the affordability of oral medications. These products are readily available in retail pharmacies, supermarkets, and increasingly online. A growing preference for treating minor illnesses at home without visiting a doctor further fuels the demand for oral OTC formulations and supports this segment.

The parenteral segment is expected to grow the fastest during the forecast period. This growth is mainly driven by the development of advanced self-injectable technologies, a rising demand for biologics, and increased self-management of chronic diseases. User-friendly injectables allow patients to safely administer treatments at home, enhancing adoption. The growth of self-administered monoclonal antibodies for autoimmune conditions and the introduction of new vaccines are also driving demand for parenteral delivery methods, which are particularly beneficial for managing specific conditions.

By Distribution Channel Analysis

The drug stores and retail pharmacies segment dominated the market in 2025, mainly due to their unmatched convenience, immediate product availability, and trusted pharmacist consultations. The extensive physical presence of pharmacies and drugstores ensures quick, on-demand access to products. Consumers, especially the aging population, value receiving immediate, professional advice from pharmacists. The high density of pharmacies enables quick and easy purchasing of medications for common ailments.

The online pharmacies segment is expected to experience the fastest growth during the forecast period. This growth is primarily due to superior convenience, increasing internet penetration, and competitive pricing. Consumers appreciate the ease of ordering, doorstep delivery, and the avoidance of in-store visits. The rise in internet usage and smartphone adoption in emerging markets has broadened access to digital health services. Online platforms often offer discounts, subscription models, and a wider range of products compared to physical retailers.

🔓 Instant Access. Zero Waiting. 📥 Buy the Premium Market Research Report Now 👉 https://www.precedenceresearch.com/checkout/1466

✚ Related Topics You May Find Useful:

➡️ Over-the-Counter Test Market: Explore how rapid self-testing solutions are transforming preventive healthcare and home-based diagnostics

➡️ Advanced Wound Care OTC Market: Discover how consumer demand for convenient wound management products is driving innovation in OTC care solutions

➡️ Over-the-Counter Analgesics Market: Analyze rising demand for accessible pain relief products amid growing self-medication trends worldwide

➡️ Antiepileptic Drugs Market: Understand how advancements in neurological therapies are improving seizure management and patient outcomes

➡️ Sedative-Hypnotic Drugs Market: Track increasing demand for sleep disorder treatments as mental wellness and stress management gain global attention

➡️ Synthetic Lethality Based Drugs and Targets Market: Gain insight into next-generation targeted cancer therapies reshaping precision oncology research

Key Government Initiatives for the Over-the-Counter (OTC) Drugs

|

Government Initiative |

Description and Impact |

|

Standalone OTC Regulatory Framework |

The CDSCO has approved recommendations to create a specific regulatory framework for OTC drugs, separating them from the general drug category to establish formal safety guidelines. |

|

Proposed OTC Drugs List |

Formulation of an initial list of 27-30 safe drugs that can be sold without a prescription, aimed at reducing self-medication risks. |

|

Sale of Select OTCs at General Stores |

An initiative to allow non-pharmacy retail outlets to sell select, safe OTC products to improve access to basic healthcare in rural areas. |

|

Jan Vishwas (Amendment) Bill, 2026 |

Decriminalized several minor infractions under the Drugs and Cosmetics Act, replacing imprisonment with monetary penalties, promoting Ease of Doing Business. |

|

Strict Pack Size and Dosage Limits |

To curb addiction and misuse, the government proposed limiting OTC pack sizes to the maximum dose recommended for five days. |

You can place an order or ask any questions, please feel free to contact at sales@precedenceresearch.com | +1 804 441 9344

Over-the-Counter (OTC) Drugs Market Companies and Their Official Product Portfolios

➢ Bayer AG: A German life sciences leader with a strong consumer health portfolio. Its OTC products include analgesics such as Aspirin, allergy and sinus remedies like Claritin™, cold and flu treatments, gastrointestinal aids, and skincare solutions. Bayer focuses on innovation, digital self-care, and expanding global access to trusted OTC products.

➢ Takeda Pharmaceutical Company Ltd.: A Japanese multinational mainly known for prescription medicines, but also offering OTC and consumer health products in select regions. Takeda focuses on digestive health, probiotics, and gastrointestinal support, expanding self-care options in Asia and Latin America.

➢ Pfizer: A U.S.-based pharmaceutical leader providing OTC products including Advil (pain relief) and digestive health remedies. Pfizer enhances its consumer health presence by collaborating with partners and converting select prescription medicines to OTC where appropriate.

➢ Johnson and Johnson Services Inc.: Through Kenvue, J&J markets OTC products such as Tylenol (pain relief), Motrin, Benadryl (allergy), and first-aid solutions. These products benefit from strong retail penetration and trusted pharmacist guidance.

➢ Sanofi S.A.: A French multinational offering OTC products like Allegra (allergy relief), Maalox (digestive aid), Theraflu/Actifed (cold and flu), and multivitamins. Sanofi invests in digital health tools and consumer wellness programs to support safe self-care.

➢ Reckitt Benckiser Group PLC: A British consumer health leader with OTC brands including Strepsils (throat lozenges), Nurofen/Disprin (pain relief), and Gaviscon (digestive care). Reckitt emphasizes everyday health, hygiene, and nutrition through innovation and strong branding.

➢ Novartis AG: A Swiss multinational primarily focused on prescription medicines, with OTC offerings available through partnerships and licensing. Products include digestive, allergy, and pain relief OTC solutions in selected markets.

➢ Boehringer Ingelheim International GmbH: German private pharma company offering OTC respiratory products such as Bisolvon and Mucosolvan in Europe, Asia, and Latin America. Boehringer emphasizes respiratory health and consumer education on safe usage.

➢ GlaxoSmithKline PLC: A UK-based company with OTC products in respiratory care (Ventolin, cough remedies), oral health (Sensodyne, Poligrip), allergy relief, and nutritional support. GSK leverages global brand recognition and R&D to meet evolving consumer health needs.

➢ Mylan: Offers generic OTC products including pain relievers, allergy medicines, and digestive health solutions. As part of Viatris, Mylan focuses on making affordable OTC products accessible globally.

Major Shifts in the Over-the-Counter (OTC) Drugs Market

🔸In March 2026, Dr. Reddy’s Laboratories launched the first-to-market generic version of Alcon’s Extra Strength Pataday (0.7% olopatadine HCl) in the U.S., offering a more affordable over-the-counter option for allergy itchy eye relief. As the first-to-market entrant, Dr. Reddy's is the first generic manufacturer to receive FDA approval and immediately sell this specific 0.7% strength formulation, distinct from recent competitor approvals. (Source: Glance Eyes on Eyecare)

🔸In July 2025, DKSH Business Unit Healthcare announced a partnership with Bayer to distribute Bayer's cardiovascular products and women's health portfolio in Singapore, Malaysia, Thailand, and the Philippines. This collaboration will implement a Distribution and Promotion alliance model, enhancing healthcare access. Ashraf Al-Ouf from Bayer highlighted DKSH's expertise and capabilities in Southeast Asia, while Bijay Singh from DKSH expressed confidence in improving patient access and ensuring compliance through this partnership. (Source: PR Newswire)

🔸In October 2025, Alfasigma announced an MX$100 million investment to establish a new over-the-counter business unit in Mexico, focusing on gastrointestinal products. This move underscores the importance of the Mexican market in Alfasigma's strategy. General Manager Vicenzo D’Elia noted positive currency stability influenced this investment, emphasizing Mexico's pharmaceutical infrastructure as a strategic hub for regional growth and talent development in Latin America. (Source: Mexico Business)

Over-the-Counter (OTC) Drugs Market Segmentation

By Product

🔸Vitamin and Dietary Supplements

🔸Cough and Cold Products

🔸Analgesics

🔸Gastrointestinal Products

🔸Sleep Aids

🔸Otic Products

🔸Wart Removers

🔸Mouth Care Products

🔸Ophthalmic Products

🔸Botanicals

🔸Smoking Cessation Products

🔸Feminine Care

🔸Others

By Route of Administration

🔸Oral

🔸Parenteral

🔸Topical

🔸Others

By Distribution Channel

🔸Drug Stores and Retail Pharmacies

🔸Hospital Pharmacies

🔸Online Pharmacies

🔸Others

By Region

🔸North America

🔸Asia Pacific

🔸Europe

🔸Latin America

🔸Middle East and Africa

Immediate Delivery Available | Buy This Premium Research Report@ https://www.precedenceresearch.com/checkout/1466

Research Methodology

🔹Primary interviews with industry experts

🔹Secondary research from company reports, regulatory databases, journals

🔹Market forecasting using top-down and bottom-up approaches

🔹Validation through triangulation models

About Us

Precedence Research is a global market intelligence and consulting powerhouse, dedicated to unlocking deep strategic insights that drive innovation and transformation. With a laser focus on the dynamic world of life sciences, we specialize in decoding the complexities of cell and gene therapy, drug development, and oncology markets, helping our clients stay ahead in some of the most cutting-edge and high-stakes domains in healthcare. Our expertise spans across the biotech and pharmaceutical ecosystem, serving innovators, investors, and institutions that are redefining what’s possible in regenerative medicine, cancer care, precision therapeutics, and beyond.

Web: https://www.precedenceresearch.com

Our Trusted Data Partners:

Towards Healthcare | Nova One Advisor | Market Stats Insight

Get Recent News:

https://www.precedenceresearch.com/news

For the Latest Update Follow Us: