From academic benches to clinical pipelines, the viral vector production (research-use) market is experiencing a rapid transformation, shifting from manual methods to automated, AI-driven platforms that reduce production timelines from months to weeks. This evolution is powered by next-generation adeno-associated virus (AAV) and lentiviral systems, as well as synthetic DNA. It addresses purification bottlenecks, thereby accelerating preclinical validation of CAR-T and CRISPR therapies and bridging the gap between molecular discovery and commercial regenerative medicine.

Viral Vector Production (Research-Use) Market Key Insights:

· The Adeno-associated virus (AAV) segment led the market with a 23.6% share in 2025.

· The lentivirus vectors segment is anticipated to grow at a rapid pace, with a CAGR of 16.2% during the forecast period.

· The gene and cell therapy development segment held the largest market share at 27.5% in 2025.

· The vaccine development segment is projected to experience significant growth, with a CAGR of 14.1%.

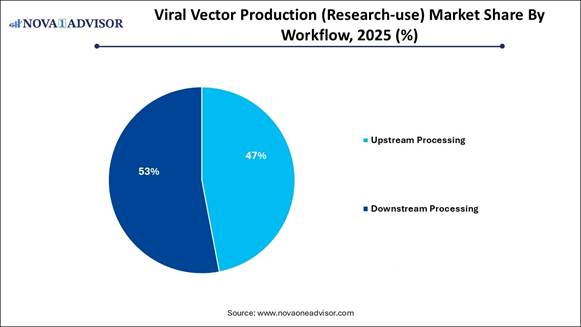

· Downstream processing dominated with the highest revenue share of 53% in 2025.

· Upstream processing is expected to grow quickly, with a CAGR of 14.3% in the forecast period.

· The pharmaceutical and biopharmaceutical segment contributed the largest revenue share at 17.4% in 2025.

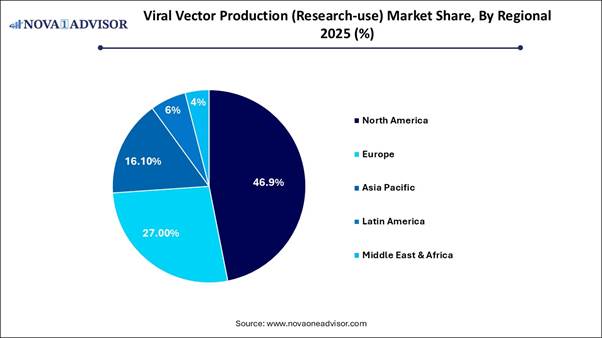

· North America held the largest share of the viral vector production (research-use) market, accounting for 46.9% in 2025.

The Complete Study is Now Available for Immediate Access | Download the Sample Pages of this Report@ https://www.novaoneadvisor.com/report/sample/8993

Market Overview: Next-Generation Viral Vectors for Gene Delivery

The Viral Vector Production (Research-use) Market focuses on manufacturing modified viruses and is fueled by a growing pipeline in cell and gene therapy, cancer research, and innovative vaccine development. Researchers are increasingly seeking high-quality modified viruses, such as AAV and lentivirus, for preclinical research and development. This sector is critical for turning experimental therapies into clinical applications and is driven by the urgent need for scalable and customized genetic delivery vehicles to treat complex disorders.

Rapid Expansion of CRISPR Screening and Functional Genomics: Major Potential

The explosive growth of functional genomics is largely propelled by high-throughput, pooled CRISPR screening using lentivirus and AAV vectors. This allows researchers to quickly unlock gene functions related to drug resistance and disease. Suppliers like VectorBuilder and Addgene are providing high-quality, custom sgRNA libraries, helping to bridge the gap between laboratory research and clinical breakthroughs.

The Hidden Cost of Batch Processing: Major Limitations

Despite the soaring demand for AAV vectors, production faces significant challenges, including high costs and low consistency. Technical complexities and a lack of standardization lead to unreliable purity and unpredictable yields, hindering preclinical reproducibility. Additionally, the prohibitively high costs put considerable financial pressure on research institutions and smaller biotech firms.

Categories and Types of Viral Vectors

- Integrating Viral Vectors (e.g., gammaretrovirus and lentivirus): These vectors integrate into the genome of the target cell, ensuring that the gene is replicated in daughter cells after mitosis.

- Non-Integrating Viral Vectors (e.g., adenovirus and adeno-associated virus): These remain episomal, meaning they do not integrate into the genome, which lowers the risk of oncogenesis.

- Non-Viral Vectors: This category includes methods like plasmid DNA, which do not involve viral particles.

In addition to these primary types, other viral vectors like alphavirus, herpesvirus, and vaccinia are also commonly used.

When selecting a viral vector, Dr. van der Loo emphasizes the importance of determining whether an integrating or non-integrating vector is required. For instance, if the target is a hematopoietic stem cell that needs to divide and produce numerous progenies, an integrating vector is preferable since the integrated gene will be passed on to the daughter cells. However, for non-dividing cells, a non-integrating vector is a better option.

Other factors to consider when choosing a viral vector include the specificity of the vector, the type of cells being targeted, and potential concerns regarding toxicity and genotoxicity.

Since the 2002 discovery that some patients treated with gammaretroviral vectors developed leukemia due to insertional mutagenesis, genotoxicity has remained a major safety concern for cell-based gene therapies. This issue is linked not only to integrating retroviral vectors but also to non-integrating vectors like AAV. While AAV vectors have shown low immunogenicity without causing acute side effects, they have triggered immunotoxicity in some clinical trials, which can hinder therapeutic effectiveness.

Finally, it's essential to assess both the in vitro and in vivo stability of the viral vector, as well as to develop safe and effective methods for producing and purifying the vector. This is where Dr. van der Loo and his team come into play.

Immediate Delivery is Available | Get Full Report Access@ https://www.novaoneadvisor.com/report/checkout/8993

Report Scope of Viral Vector Production (Research-use) Market

|

Report Coverage |

Details |

|

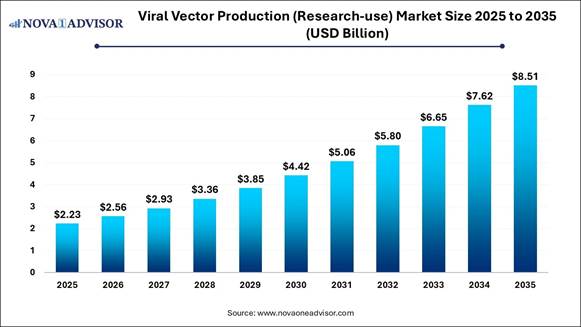

Market Size in 2026 |

USD 2.56 Billion |

|

Market Size by 2035 |

USD 8.51 Billion |

|

Growth Rate From 2026 to 2035 |

CAGR of 14.33% |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2035 |

|

Segments Covered |

By Vector Type, By Workflow, By Application, By End use |

|

Market Analysis (Terms Used) |

Value (USD Million/Billion) or (Volume/Units) |

|

Regional Covered |

North America, Europe, Asia Pacific, Latin America, MEA |

|

Key Companies Profiled |

Merck KGaA; Lonza; FUJIFILM Diosynth Biotechnologies.; Cobra Biologics Ltd; Thermo Fisher Scientific, Inc.; Waisman Biomanufacturing; Genezen; YPOSKESI, Inc; Advanced BioScience Laboratories, Inc. (ABL, Inc); Novasep Holdings SAS; Orgenesis Biotech Israel Ltd (formerly ATVIO Biotech ltd.); Vigene Biosciences, Inc. |

For more information, visit the Nova One Advisor website or email the

team at sales@novaoneadvisor.com |

Call us: +1 804 420 9370 Viral Vector Production (Research-use)

Market: Regional Analysis North America dominated the market in 2025

due to its high concentration of biotech firms, significant investment in

research and development, and the rapid adoption of advanced gene and cell therapies.

Major CDMOs like Thermo Fisher Scientific, Lonza, Catalent, and Charles River

Laboratories are based in North America, offering scalable manufacturing

services. The FDA supports faster development and increased demand for gene

therapy products through favorable fast-track and accelerated

designations that enhance research in advanced therapies. The U.S. leads the global market, driven by

its advanced CDMO infrastructure, high-volume AAV and lentiviral production,

and unparalleled research and development funding. The surge in demand for gene

therapies and post-COVID vaccine innovations has solidified the nation’s

position as a leader in next-generation genetic medicine. ·

In September 2025, Thermo Fisher Scientific

announced a partnership with South Korea’s Dr. Park CDMO to establish a new

facility equipped with advanced technologies for high-capacity, cGMP-compliant

viral vector production. This collaboration aims to enhance global access to

next-generation cell and gene therapies. Canada is rapidly emerging as a global

leader in this market, leveraging strong government-backed research and

development alongside specialized CDMO partnerships to drive innovation in gene

delivery. By combining robust academic research with growing GMP-compliant

manufacturing capabilities, accelerating the commercialization of high-quality

vector production for life-saving gene and cell therapies. Asia Pacific region is experiencing the

fastest growth during this forecast period, driven by a surge in gene therapy

research, substantial investments in biotechnology,

and strong government support. There is a notable increase in preclinical and clinical

trials, particularly in China and Japan, which require high-quality

viral vectors for therapeutic gene delivery. Enhancements in AAV and lentiviral

production techniques have improved efficiency, making these vectors the

preferred choice for research. Significant capital inflows from private and

government sectors are facilitating the establishment of advanced GMP-certified

production facilities. India is rapidly evolving into a global

high-tech hub, positioning itself as the fastest-growing market for viral

vectors, plasmid DNA, and advanced biologics.

By leveraging its cost-efficient and skilled manufacturing workforce, India is

transitioning from being a leader in vaccine production, as seen with

breakthroughs like ZyCoV-D, to pioneering advancements in gene therapy and

targeted biotherapeutics. ·

In February 2026, the Union Budget 2026-27

launched Biopharma SHAKTI, a ₹10,000 crore, five-year initiative designed to

transform India into a global powerhouse for biologics and biosimilars

production. Fueled by massive state backing and a surge

in clinical trials for rare diseases and oncology,

China is accelerating its dominance in the market. Major players like WuXi

AppTec, GenScript ProBio, and ASKBio China are establishing massive

GMP-certified CDMO hubs, offering high-throughput AAV and lentiviral vector

production that couples next-generation manufacturing technology with lower

costs to dominate global supply chains. Buy Now Full Report: https://www.novaoneadvisor.com/report/checkout/8993

Viral Vector Production (Research-use)

Market: Segment Insights By Vector Type Analysis The Adeno-associated

Virus (AAV) segment dominated the market in 2025, primarily due to its

exceptional safety profile, low immunogenicity, and broad tissue tropism for

gene therapy. AAV vectors are highly favored for gene therapy research because

they cannot replicate independently and integrate into the host genome only

rarely, ensuring high safety. There is also an increasing pipeline of gene

therapies, particularly targeting rare and neurological disorders. The

transition from adherent to suspension-based cell culture systems provides

improved production yields and lower costs, enhancing scalability. The lentivirus segment is expected to

experience the fastest growth during the forecast period, driven mainly by the

increasing demand for CAR-T therapy development, gene editing, stem cell

engineering, and advanced scalable production technologies. New scalable

production systems enable efficient, large-scale production, progressing from

initial research to clinical development. Lentiviruses are extensively utilized

for complex gene circuits, shRNA libraries, and CRISPR components, supporting

immunotherapy research and the creation of personalized immune therapies. By Application Analysis The cell and gene therapy development

segment led the market in 2025, primarily due to the need to optimize gene

therapy candidates, rising investments in advanced medicine, and the expansion

of cancer-focused immunotherapy research. The surge in development for advanced

treatments, including CAR-T therapies and genetic disorder treatments, has

prompted researchers to invest heavily in custom vector design. This has generated

a high demand for research-grade vectors on a small-to-large scale for

specialized vector production services, particularly in oncology. The vaccine development segment is

anticipated to grow the fastest during the forecast period. This growth is

primarily attributed to increasing investments in gene therapies, rapid

advancements in upstream processing efficiency, and the necessity for a quick

response to emerging infectious diseases. The rising prevalence of infectious

diseases, alongside the urgent need for new cancer treatments, is driving

research-focused production. Innovations such as serum-free media, improved

transfection reagents, and advancements in bioreactor technology enable faster

and more scalable research-grade vector production. By Workflow Analysis The downstream

processing segment held a dominant market position in 2025, mainly due

to the critical demand for high-purity vectors, which maximize transfection efficiency

and minimize toxicity in research, preclinical, and clinical applications. This

process involves intricate, expensive, and time-consuming steps, such as chromatography

and ultrafiltration, to remove host cell proteins and nucleic acids,

generating substantial revenue. Advancements in downstream technologies are

required to overcome bottlenecks and improve recovery rates. The upstream processing segment is projected

to experience the fastest growth during the forecast period. This growth

results from the adoption of single-use bioreactors, optimized cell culture

technologies, and advanced transfection methods. The increased use of

single-use bioreactors enhances flexibility and reduces contamination risks,

which is essential for accelerating production timelines. Innovations in cell

line development, particularly with suspension cell culture systems, allow for

higher yields and scalability compared to adherent systems, thereby improving

vector amplification efficiency. By End Use Analysis The pharmaceutical

and biopharmaceutical

companies segment led the market in 2025, primarily due to high-volume demand

stemming from expanding gene and cell therapy pipelines, significant

investments in research and development, and the need for optimized, scalable

production platforms. There is a growing focus on developing advanced therapies

for various diseases, which necessitates high-quality, efficient vector

production. Companies are engaging in collaborations, acquisitions, and

partnerships with contract research organizations to accelerate development

times and secure expertise in vector design, driving overall market growth. The research institutes segment is

anticipated to grow the fastest during the forecast period. This growth is

driven by the expansion of academic, government, and preclinical studies in

gene and cell therapy. Research institutes serve as primary hubs for

early-stage discovery, developing experimental therapies for cancer, rare

genetic diseases, and neurological disorders using viral vectors. Increasing

investments from government grants and partnerships with biotechnology startups

for technology transfer, pilot-scale production, and early-stage trials

necessitate the availability of high-grade vectors for specialized laboratory

applications. Viral Vector Production (Research-use)

Market Companies ·

Lonza ·

FUJIFILM Diosynth Biotechnologies U.S.A., Inc. ·

Charles River Laboratories. ·

Waisman Biomanufacturing ·

Genezen ·

Yposkesi,Inc. ·

Advanced BioScience Laboratories, Inc. (ABL,

Inc.) Key Emerging Innovations in the Viral

Vector Production (Research-use) Market Innovation Technology Focus Area Synthetic DNA Alternatives Enzymatically produced linear synthetic DNA (e.g., 4basebio) Upstream: Replacing expensive, variable plasmid DNA to reduce cost

and impurities. Suspension Cell Culturing HEK293 suspension systems (e.g., in 50L–5,000L bioreactors) Upstream: Transitioning from adherent to suspension for better scalability

and higher yield. AI-Driven Vector Design AI/ML-guided capsid optimization (e.g., Evo 2, StripedHyena) Vector Design: Optimizing promoters and tropism for

high-throughput engineering. Closed Automated Systems Single-use bioreactors and automated purification (e.g., Scale-X,

Sartorius) Downstream: Improving reproducibility and sterility while reducing

labor. Serotype-Agnostic Purification Affinity chromatography/Nanofiber adsorbents (e.g., AAVX ligands) Downstream: Improving separation of full capsids from empty ones

efficiently.

Major Shifts in the Viral Vector

Production (Research-use) Market ·

In May 2025, AGC Biologics partnered with Quell

Therapeutics to advance T-Regulatory cell therapies for immune disorders. AGC

will provide lentiviral vector (LVV) material using its ProntoLVV™ platform for

CTA/IND submissions, producing LVV material at its Milan facility. This

collaboration aims to streamline development and ensure GMP readiness for

Quell's Treg therapies. ·

In November 2025, AGC announced a new

manufacturing agreement with AAVantgarde to produce Good Manufacturing Practice

(GMP) materials for two novel adeno-associated virus (AAV) candidates aimed at

treating progressive vision loss: AAVB-039 for Stargardt disease and AAVB-081

for retinitis pigmentosa. This partnership enhances AAVantgarde's gene therapy

pipeline. ·

In November 2025, Bharat Biotech launched

Nucelion Therapeutics, a CRDMO focused on cell and gene therapy, based in

Genome Valley. With a 30,000 sq. ft. GMP facility, Nucelion aims to fill gaps

in India's CGT manufacturing and meet international demand for advanced

biological therapies. Related Report – ➡️ Viral Capsid Development Market Segments Covered in the Report This report forecasts revenue growth at

country levels and provides an analysis of the latest industry trends in each

of the sub-segments from 2026 to 2035. For this study, Nova one advisor, Inc.

has segmented the viral vector production (research-use) market By Vector Type By Application By Workflow By End Use Regional Immediate Delivery

Available | Buy This Premium Research https://www.novaoneadvisor.com/report/checkout/8993 About-Us Nova One Advisor is a global leader

in market intelligence and strategic consulting, committed to delivering deep,

data-driven insights that power innovation and transformation across

industries. With a sharp focus on the evolving landscape of life sciences, we

specialize in navigating the complexities of cell and gene therapy, drug

development, and the oncology market, enabling our clients to lead in some of

the most revolutionary and high-impact areas of healthcare. Our expertise spans the entire

biotech and pharmaceutical value chain, empowering startups, global

enterprises, investors, and research institutions that are pioneering the next

generation of therapies in regenerative medicine, oncology, and precision

medicine. Web: https://www.novaoneadvisor.com/ Our Trusted Data Partners: Nova One Advisor - Market

Research Reports & Consulting Firm Nova One Advisor offers

comprehensive market research reports with in-depth industry analysis and

market data. Call us: +1 804 420 9370 Email: sales@novaoneadvisor.com Web: https://www.novaoneadvisor.com/ You can place an order or ask any

questions, please feel free to contact at sales@novaoneadvisor.com | +1 804 441 9344

➡️ Cell Therapy Human Raw Materials Market

➡️ Scaffold-free 3D Cell Culture Market

➡️ U.S. Anatomic Pathology Market

➡️ U.S. Antiviral Drugs Market

➡️ U.S. Cell And Gene Therapy Clinical Trials Market

➡️ Gynecological Cancer Drugs Market

➡️ U.S. Clinical Laboratory Services Market

➡️ CRISPR-based Gene Editing Market

➡️ Nanotechnology

Market

➡️ RNA Therapeutics Market

➡️ Biobanking

Market

➡️ Immunofluorescence Assay Market

➡️ Cell and Gene Therapy Market

➡️ Viral Vector And Plasmid DNA Manufacturing Market

➡️ Radiation Oncology Market

➡️ U.S. Generic Drugs Market

➡️ Active Pharmaceutical Ingredients CDMO Market

➡️ Implantable Medical Devices Market

➡️ Single-use Bioprocessing Market

➡️ U.S. Single-use Bioprocessing Market

➡️ Advanced Therapy Medicinal Products CDMO Market

➡️ AI In Healthcare Market