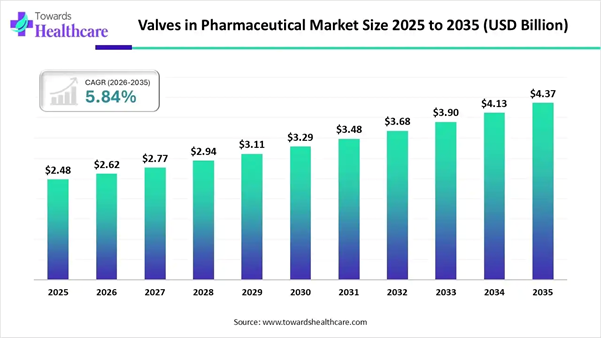

The global valves in pharmaceutical market size was estimated at USD 2.48 billion in 2025 and is predicted to increase from USD 2.62 billion in 2026 to approximately USD 4.37 billion by 2035, expanding at a CAGR of 5.84% from 2026 to 2035.

The Complete Study is Now Available for Immediate Access | Download the Free Sample Pages of this Report @ https://www.towardshealthcare.com/download-sample/6706

With the rising average age of the World’s population, the need for new medications and progressive production processes in the pharmaceutical industry is also rising. Diaphragm valves play a major role in securing contamination-free and efficient production. Moreover, the rising living standards in countries like China, India, and the Asia Pacific region are also raising the need for medications. Valves such as KSB’s SISTO-C diaphragm valve are playing a crucial role in providing accurate control in the production processes of biologics, including filtration, centrifugation, chromatography, protein processing, and sterile formulations. The complex nature of the production processes of biologics placed high demands on valves.

The Valves in Pharmaceutical Market: Highlights

• The valves in pharmaceutical market will likely exceed USD 2.62 billion by 2026.

• Valuation is projected to hit USD 4.37 billion by 2035.

• Estimated to grow at a CAGR of 5.84% starting from 2026 to 2035.

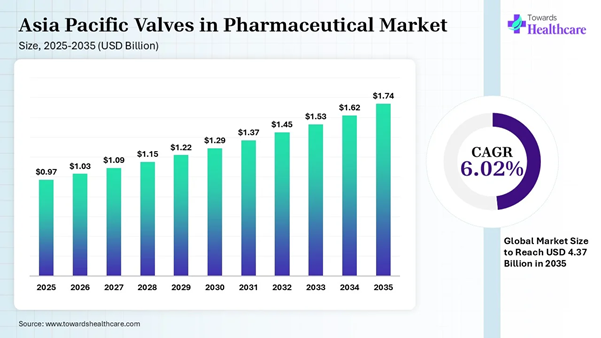

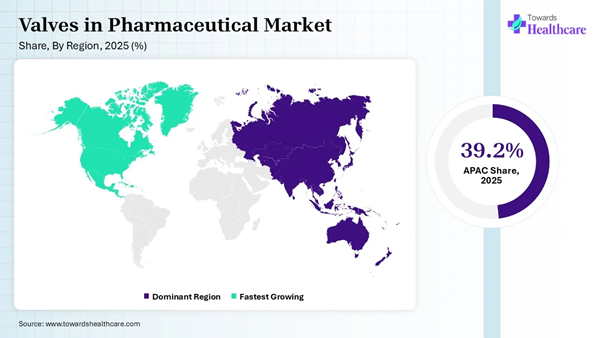

• Asia Pacific held the major revenue share of 39.2% in the global valves in pharmaceutical market in 2025.

• North America is expected to be the fastest-growing region between 2026 and 2035.

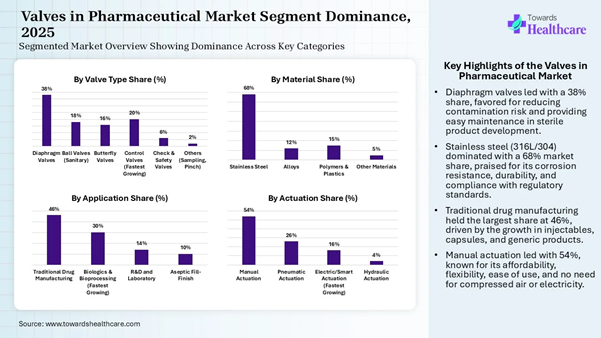

• By valve type, the diaphragm valves segment held a major share of 38% in the market in 2025.

• By valve type, the control valves segment is expected to be the fastest growing during the forecast period.

• By material type, the stainless steel segment dominated the market by 68% in 2025.

• By material type, the polymers & plastics segment is expected to be the fastest-growing during the forecast period.

• By application type, the traditional drug manufacturing segment led the market by 46% in 2025.

• By application type, the biologics & bioprocessing segment is expected to be the fastest growing during the forecast period.

• By actuation type, the manual actuation segment dominated the market share by 54% in 2025.

• By actuation type, the electric/smart actuation segment is expected to be the fastest growing during the forecast period.

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Market Overview

Valves in Pharmaceutical: Achieving Precise Control Over Complex Processes

The modern and fully automated bioreactors need valves that can be integrated into a process control system to monitor and control all production processes precisely. Valves in pharmaceutical market also contribute to the accurate control over the content of oxygen, CO2, and nutrients in the bioreactors. They avoid the risk of any fluctuations that could impact the quality of medicines produced and impair the growth of cells. The pharmaceutical industry needs to pay keen attention to hygiene, self-draining ability, cleanability, suitable materials, and zero dead volume for pharmaceutical valves.

However, the pharmaceutical industry needs to meet high-quality standards during production to ensure the required surface quality. To meet the cleaning and sterility requirements, pharmaceutical systems are subjected to validation processes, including guidelines of the International Society for Pharmaceutical Engineering (ISPE) or the Good Manufacturing Practices (GMP) of the European Union.

The Valves in Pharmaceutical Market: Regional Analysis

|

Region |

Share (%) |

|

Asia Pacific |

39.2 |

|

North America (Fastest Growing) |

26 |

|

Europe |

22 |

|

Latin America |

6 |

|

Middle East & Africa (MEA) |

6.8 |

• Asia Pacific dominates the market with a

39.2% share, driven by rapid industrial growth, increasing healthcare

investments, and the manufacturing base in countries like China and India. • North America (Fastest Growing) growing

rapidly with a 26% share, fueled by advancements in healthcare technology,

increasing demand for medical devices, and strong research and development

activities. • Europe accounts for 22% of the market,

with a well-established healthcare system, strong regulatory standards, and a

growing focus on medical innovations. • Latin America holds 6% of the market,

growing slowly with increased healthcare access and rising investments in

medical technology across the region. • Middle East & Africa (MEA) represents

6.8% of the market, driven by improvements in healthcare infrastructure and

rising healthcare demand, though still a smaller share compared to other

regions. Massive Manufacturing Facilities Drive

Asia Pacific Asia Pacific dominated the market in 2025,

owing to a shift towards biologics and complex therapies, and the increased

adoption of single-use manufacturing systems. The Asia Pacific is positioned as

a pivotal biopharmaceutical

hub in 2025, driven by strategic investments, robust innovation, and

evolving healthcare needs. The rising trend of global collaborations led

pharmaceutical companies towards more licensing and co-development deals for

novel therapeutics. Policy shifts aim to improve the regional clinical research

and regulatory environment. For instance, research by the United

Nations suggests that the number of people older than 65 years will have risen

to 2.2 billion by 2070. This development will lead to an increased number of

people with non-infectious diseases, including cancer and diabetes. India Market Analysis The valves in pharmaceutical market in

India is witnessing the increased production

of biosimilars, complex generics, and innovative drugs, and increased

investments in biotechnology innovations. The Biotechnology Industry Research

Assistance Council (BIRAC) of the government fuels early-stage innovation

through equity investments, grants, and low-interest loans to startups. For instance, studies implied that global

demand for medications has increased by 14% in the last five years, and is

projected to rise by another 12% by 2028. It has raised the need for new

medication approaches and reliable and safe production processes. North America is expected to grow at the

fastest rate in the valves in pharmaceutical market during the forecast period

due to the rise of novel therapies and biologics, supply chain resilience, and

regulatory compliance. North American government initiatives impact the demand

and regulation for high-performance valves used in pharmaceutical

manufacturing. These government programs prioritize supply chain resilience and

advanced manufacturing technologies. The continued efforts towards automation

and modernization drive the North

American market for valves in pharmaceutical. For instance, • In November 2024, ICU Medical, Inc. and

Otsuka Pharmaceutical Factory, Inc. announced the creation of a joint venture

to boost the manufacturing and innovation in IV solutions, like IV pumps and

consumables, in North America. They have networked with a combined production

of an estimated 1.4 billion annual units and aim to boost supply chain

resiliency in North America. U.S. Market Trends The valves in pharmaceutical market in the

U.S. is experiencing stricter hygiene and regulatory standards, the adoption of

automation and Industry 4.0, and the expansion of biopharmaceutical manufacturing.

The U.S. FDA introduced the breakthrough devices program, which is a voluntary

program for certain device-led combination products and medical devices that

offer more effective diagnosis or treatment. For instance, • In April 2025, Fujifilm Biotechnologies

announced its plan to launch the new manufacturing plant in the U.S., with

Regeneron and Johnson & Johnson as initial customers. Lars Petersen, CEO of

Fujifilm Biotechnologies, reported that there was a strong focus on achieving

extreme hygiene and a high technology level in this pharmaceutical

manufacturing facility for the safety of patients. Get the latest insights on life science

industry segmentation with our Annual Membership: https://www.towardshealthcare.com/get-an-annual-membership The Valves in Pharmaceutical Market:

Segmentation Analysis Valve Type Insights Segment Share (%) Diaphragm Valves 38% Ball Valves (Sanitary) 18% Butterfly Valves 16% Control Valves (Fastest

Growing) 20% Check & Safety Valves 6% Others (Sampling, Pinch) 2%

• Diaphragm Valves dominates the market

with a 38% share due to their precise control, leak-proof nature, and

widespread use in sanitary and biopharmaceutical applications. • Control Valves gaining momentum with a

20% share, driven by their critical role in regulating flow and pressure in

various industries, including healthcare and manufacturing. • Ball Valves holds 18% of the market,

valued for their durability and sanitary design, commonly used in

pharmaceutical and food processing industries. • Butterfly Valves accounts for 16%,

popular for their compact design and efficiency in controlling large volumes of

fluid, but not as dominant as diaphragm and control valves. • Check & Safety Valves represents 6%

of the market, crucial for preventing backflow and ensuring system safety,

though they occupy a smaller share compared to other valve types. • Others holds 2% of the market, covering

niche applications such as sample handling and fluid isolation, with a smaller

share due to their specialized use. The diaphragm valves segment dominated

the market in 2025, owing to the use of a flexible diaphragm to control the

flow of a gas, liquid, or steam through a pipeline. It acts as the closing

element to block the flow, while the lifting up of a diaphragm allows the fluid

to pass through. The diaphragm valves possess a non-contaminating design, which

makes them ideal in sterile or clean process applications like pharmaceuticals.

The control valves segment is expected to

be the fastest-growing in the valves in pharmaceutical market during the

forecast period due to the importance of control valves in pharmaceutical

industry. They feature precise process control, flexibility in production,

batch-to-batch consistency, and optimization of energy and resources. They are

vital in the production of a wide range of medications and medical products that

improve and sustain human health. Material Type Insights Segment Share (%) Stainless Steel (316L/304) 68 Alloys (Hastelloy/Monel) 12 Polymers & Plastics

(PTFE/PFA) (Fastest Growing) 15 Other Materials 5

• Stainless Steel (316L/304) dominates the

market with a 68% share, favored for its strength, corrosion resistance, and

widespread use in medical, pharmaceutical, and food processing industries. • Polymers & Plastics gaining momentum

with a 15% share, driven by their flexibility, chemical resistance, and rapid

adoption in various industries, including healthcare and biopharmaceuticals. • Alloys (Hastelloy/Monel) holds 12% of

the market, valued for their resistance to extreme environments and used in

high-performance applications, though not as dominant as stainless steel. • Other Materials represents 5% of the

market, encompassing a range of specialized materials used in niche

applications, but with a smaller share due to their limited use compared to the

primary materials. The stainless steel segment dominated

the market in 2025, owing to the most popular types of stainless steel, such as

316L and 304, for pharmaceuticals. The 316L type plays a role in pharmaceutical

equipment and process piping. The 304 type of material is resistant to

corrosion and shows ease of fabrication and welding. The 304 material is used

for storage tanks, pharmaceutical equipment, and piping. The polymers & plastics segment is

expected to be the fastest-growing in the valves in pharmaceutical market

during the forecast period due to their cost-effectiveness, versatility, and

durability. These materials

are used in packaging, medical devices, storage, and transportation.

They play a critical role in ensuring the efficacy, safety, and accessibility

of pharmaceutical products. Application Type Insights Segment Share (%) Traditional Drug Manufacturing 46 Biologics & Bioprocessing (Fastest Growing) 30 R&D and Laboratory 14 Aseptic Fill-Finish 10

• Traditional Drug Manufacturing dominates

the market with a 46% share, driven by the ongoing demand for mass production

of generic and over-the-counter drugs. • Biologics & Bioprocessing gaining

momentum with a 30% share, fueled by the increasing demand for biologics and

biopharmaceuticals, along with advancements in bioprocessing technologies. • R&D and Laboratory accounts for 14%

of the market, focusing on the development and testing of new drugs, but does

not dominate as much compared to traditional manufacturing and biologics. • Aseptic Fill-Finish represents 10% of

the market, crucial for the sterile packaging of biologics and pharmaceuticals,

though it occupies a smaller share compared to the larger segments. The traditional drug manufacturing segment

led the market in 2025, owing to the participation of multiple funding

mechanisms and partners in the drug research and development process. The drug

development and approval process is pivotal due to pre-clinical studies, an

investigational new drug (IND) request with the FDA, clinical

trials, NDA filing with the FDA, and post-market safety monitoring. FDA

reviewers pay attention to proposed labelling, safety updates, drug abuse

information, patent information, and directions for use. The biologics & bioprocessing segment

is expected to be the fastest-growing in the valves in pharmaceutical market

during the forecast period due to the transformation of modern pharmaceuticals

by bioprocessing. Bioprocessing uses biological materials, such as cells and

enzymes, to create products like vaccines,

medicines, bioenergy, and biofuels. On the other hand, biologics are

large-molecule drugs produced from living cells, which are the fastest-growing

sectors of the pharmaceutical industry. Actuation Type Insights Segment Share (%) Manual Actuation 54 Pneumatic Actuation 26 Electric/Smart Actuation

(Fastest Growing) 16 Hydraulic Actuation 4

• Manual Actuation dominates the market

with a 54% share, preferred for its simplicity, reliability, and

cost-effectiveness in a wide range of applications. • Pneumatic Actuation holds 26% of the

market, valued for its speed, ease of use, and reliability, particularly in

automation and process control industries. • Electric/Smart Actuation (Fastest

Growing) gaining momentum with a 16% share, driven by advancements in smart

technology and automation, offering higher precision, control, and energy

efficiency. • Hydraulic Actuation represents 4% of the

market, typically used in high-force applications, but with a smaller share

compared to pneumatic and manual actuation due to its complexity and cost. The manual actuation segment dominated

the market in 2025, owing to its immense role in providing flexibility, safety,

and reliability in specific conditions. Manual systems offer reliability and

simplicity, where human intervention is convenient. The medical

devices, like nasal pumps, can be actuated manually during product

development to study the initial mechanics of drug delivery. The electric/smart actuation segment is

expected to be the fastest-growing in the valves in pharmaceutical market

during the forecast period due to the shift towards electric actuators, driven

by lower maintenance and energy efficiency. They offer enhanced safety and easy

integration, including valve control and monitoring. They can be controlled

remotely, which reduces human exposure to hazardous environments. Become a valued research partner with us

- https://www.towardshealthcare.com/schedule-meeting The Valves in Pharmaceutical Market

Companies • Emerson Electric Co. • Alfa Laval AB • Bürkert Fluid Control Systems • Flowserve Corporation • Spirax-Sarco Engineering plc • GEMÜ Group • Crane Co. • Swagelok Company • Parker-Hannifin Corporation • Velan Inc. Segments Covered in the Report By Valve Type • Diaphragm Valves • Ball Valves (Sanitary) • Butterfly Valves • Control Valves • Check & Safety Valves • Others (Sampling, Pinch) By Material • Stainless Steel (316L/304) • Alloys (Hastelloy/Monel) • Polymers & Plastics (PTFE/PFA) • Other Materials By Application • Traditional Drug Manufacturing • Biologics & Bioprocessing • R&D and Laboratory • Aseptic Fill-Finish By Actuation • Manual Actuation • Pneumatic Actuation • Electric/Smart Actuation • Hydraulic Actuation By Region • North America • South America • Europe • Asia Pacific • MEA Immediate Delivery Available | Buy This

Research Report Now @ https://www.towardshealthcare.com/checkout/6706 Access our comprehensive healthcare

dashboard for detailed market insights, segment breakdowns, regional

performance, and company profiles: https://www.towardshealthcare.com/access-dashboard About Us Towards Healthcare is a leading global provider of technological solutions, clinical

research services, and advanced analytics, with a strong

emphasis on life science research. Dedicated to

advancing innovation in the life sciences sector, we build strategic

partnerships that generate actionable insights and transformative

breakthroughs. As a global strategy consulting firm, we empower life science

leaders to gain a competitive edge, drive research excellence, and accelerate

sustainable growth. You can place an order or ask any

questions, please feel free to contact us at sales@towardshealthcare.com Europe Region: +44 778 256 0738 North America Region: +1 8044 4193 44 APAC Region:

+91 9356 9282 04 Web: https://www.towardshealthcare.com Our Trusted Data Partners Precedence

Research | Towards Packaging | Towards

Food and Beverages | Towards

Chemical and Materials | Towards Dental | Towards EV Solutions | Healthcare Webwire Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest Browse More Insights of Towards

Healthcare: ➡️The global pharmaceutical

ERP market was valued at USD 2.96 billion in

2025 and is forecasted to grow from USD 3.33 billion in 2026 to USD 9.66

billion by 2035, at a CAGR of 12.56% from 2026 to 2035. ➡️The global pharmaceutical

grade melatonin market is projected to reach

USD 1044.3 million by 2034, up from USD 479.9 million in 2024 and USD 521

million in 2025, expanding at a CAGR of 8.56% between 2025 and 2034. ➡️The global pharmaceutical

CDMO market was valued at USD 167.96 billion in

2025 and is expected to grow to USD 337.89 billion by 2035, with a CAGR of

7.24% from 2026 to 2035. ➡️The global pharmaceutical

excipients market, valued at USD 10.83 billion

in 2025, will increase to USD 16.12 billion by 2035, growing at a CAGR of 4.06%

from 2026 to 2035. ➡️The global pharmaceutical

filtration market, valued at USD 14.95 billion

in 2025, is expected to reach USD 32.51 billion by 2035, growing at a CAGR of

8.08% during the forecast period from 2026 to 2035. ➡️The global pharmaceutical

spray drying market is forecasted to grow from

USD 2.55 billion in 2025 to USD 4.93 billion by 2034, expanding at a CAGR of

7.67% between 2025 and 2034. ➡️The global pharmaceutical

CRO and CDMO market, valued at USD 254.65

billion in 2025, will grow to USD 594.07 billion by 2035, at a CAGR of 8.84%

from 2026 to 2035. ➡️The global pharmaceutical

testing services market, projected to reach USD

12.86 billion by 2035 from USD 5.22 billion in 2026, is growing at a CAGR of

10.54% from 2026 to 2035. ➡️The global pharmaceutical

water market was valued at USD 38.70 billion in

2023 and is expected to reach USD 107.15 billion by 2034, with a CAGR of 9.25%

from 2024 to 2034. ➡️The global pharmaceutical

intermediate CDMO market, valued at USD 43.45

billion in 2025, is forecasted to grow to USD 89.72 billion by 2035, expanding

at a CAGR of 7.52% from 2026 to 2035.