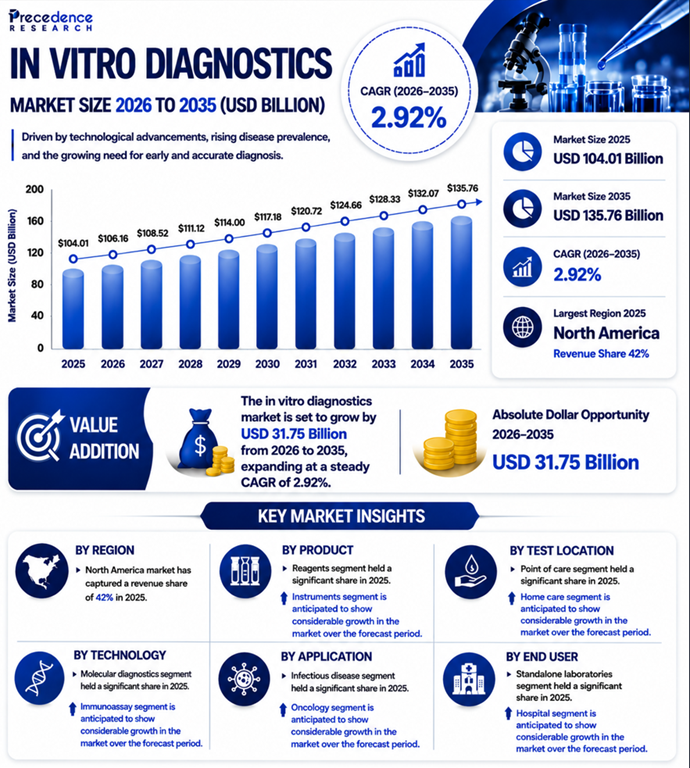

The global in vitro diagnostics (IVD) market is projected to grow from USD 106.16 billion in 2026 to nearly USD 135.76 billion by 2035, with a CAGR of 2.7% from 2026 to 2035. The market growth is fueled by rising demand for decentralized diagnostics, increasing adoption of precision medicine, rapid expansion of molecular testing technologies, and growing integration of artificial intelligence into clinical workflows.

The

U.S. In

Vitro Diagnostics market

is entering a transformative era. AI-driven molecular testing, point-of-care

platforms, and home-based diagnostics are enabling faster, more accurate, and

personalized disease detection. With projected growth from USD 35.43 billion in 2025 to USD 43.49 billion by 2035, the market is redefining

how healthcare delivers timely and life-saving insights.

Where Data Meets Strategic Clarity 📥 View Sample Pages of

the Complete Report 👉 https://www.precedenceresearch.com/sample/1130

From centralized laboratory workflows to decentralized patient care, the in vitro diagnostics (IVD) market is experiencing a significant digital transformation. This shift is moving away from manual, high-volume testing towards automated, intelligent, and personalized diagnostic solutions. With the help of AI-enabled digital pathology, molecular diagnostics, and cloud-connected point-of-care devices, diagnostic turnaround times are being reduced from days to minutes. This advancement transforms early detection into a reliable standard for high-precision clinical care in oncology and chronic disease management.

The future of diagnostics is shifting from centralized laboratory systems toward intelligent, decentralized, and patient-centric testing ecosystems,” said Rohan Patil a Principal Consultant at Precedence Research. “AI-assisted diagnostics, next-generation sequencing, and rapid molecular testing are transforming how healthcare providers detect, monitor, and manage diseases in real time.

In Vitro Diagnostics Market Key Insights

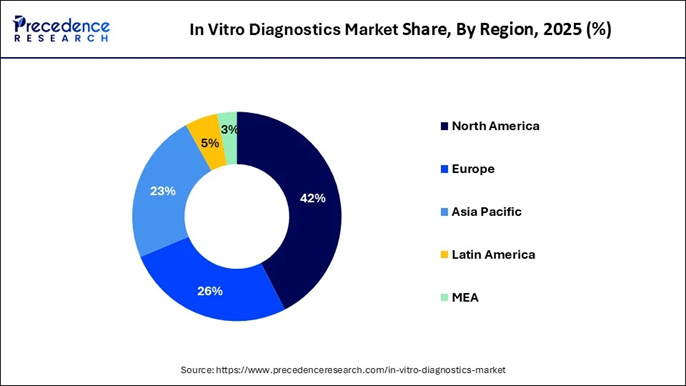

🔹North America dominated with the largest market share of 42% in 2025.

🔹Asia Pacific is anticipated to have the fastest growth with a notable CAGR during the forecast period.

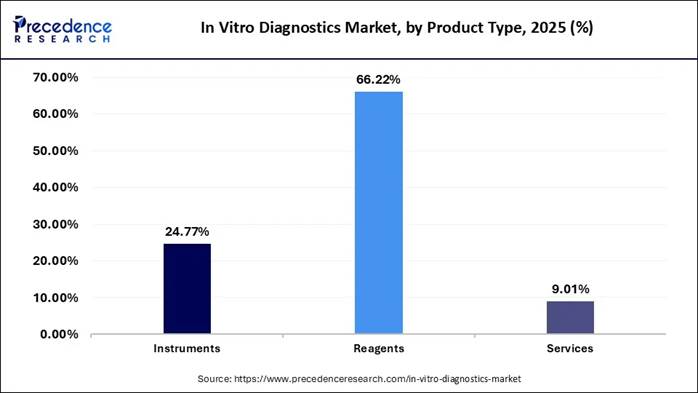

🔹By product, the reagents segment contributed the highest market share in 2025.

🔹By product, the instruments segment is growing at a strong CAGR between 2026 and 2035.

🔹By test location, the point-of-care testing segment held a major market share in 2025.

🔹By test location, the home care segment is expected to expand at a notable CAGR from 2026 to 2035.

🔹By technology, the molecular diagnostics segment captured the highest market share in 2025.

🔹By technology, the immunoassay segment is poised to grow at a healthy CAGR between 2026 and 2035.

🔹By application, the infectious disease segment generated the biggest market share in 2025.

🔹By application, the oncology segment is expanding at the fastest CAGR between 2026 and 2035.

🔹By end user, the standalone laboratories segment accounted for the largest market share in 2025.

🔹By end user, the hospital segment is projected to grow at a solid CAGR between 2026 and 2035.

See Where the Market Is Headed Next 👉 https://www.precedenceresearch.com/in-vitro-diagnostics-market

Global In Vitro Diagnostics (IVD) Market Revenue Analysis by Segments 2023-2025

Global IVD Market Revenue (USD Million), By Product Type, 2023-2025

|

Product |

2023 |

2024 |

2025 |

|

Instruments |

26,909.55 |

25,379.75 |

25,765.08 |

|

Reagents |

70,996.28 |

67,404.76 |

68,879.13 |

|

Services |

9,861.36 |

9,264.58 |

9,366.26 |

Global IVD Market Revenue (USD Million), By Technology, 2023-2025

|

Technology |

2023 |

2024 |

2025 |

|

Immunoassay |

32,433.72 |

30,774.22 |

31,428.44 |

|

Hematology |

6,345.41 |

5,984.69 |

6,075.32 |

|

Clinical Chemistry |

18,978.14 |

18,061.02 |

18,500.19 |

|

Molecular Diagnosis |

35,662.26 |

33,736.25 |

34,350.28 |

|

Coagulation |

4,328.27 |

4,061.72 |

4,102.53 |

|

Microbiology |

5,916.29 |

5,563.15 |

5,630.39 |

|

Others |

4,103.12 |

3,868.03 |

3,923.34 |

Global IVD Market Revenue (USD Million), By Application, 2023-2025

|

Application |

2023 |

2024 |

2025 |

|

Infectious Diseases |

56,833.27 |

53,602.44 |

54,414.15 |

|

Diabetes |

8,475.36 |

7,969.48 |

8,065.80 |

|

Oncology |

8,323.38 |

8,055.14 |

8,390.58 |

|

Cardiology |

8,538.03 |

8,125.43 |

8,323.01 |

|

Nephrology |

6,127.88 |

5,744.71 |

5,796.57 |

|

Autoimmune Diseases |

4,987.83 |

4,718.45 |

4,804.33 |

|

Drug Testing |

3,757.30 |

3,593.52 |

3,699.21 |

|

Others |

10,724.14 |

10,239.92 |

10,516.82 |

Market Overview: The Unsung Hero of Rapid Disease Detection

The global IVD market is thriving as a cornerstone of modern healthcare, enabling rapid and accurate disease detection outside the body through advanced molecular diagnostics, immunoassay methods, and point-of-care testing. The growth is driven by an aging population, a rise in chronic diseases, and a swift shift toward personalized precision medicine. This often-overlooked segment of medical devices, which includes laboratory instruments and rapid test kits, is witnessing explosive demand for faster turnaround times and high-precision results, effectively steering the industry from traditional diagnostics to intelligent, data-driven, and decentralized care.

Beyond disease detection, the IVD industry is increasingly becoming the backbone of predictive and preventive healthcare. Advanced diagnostic technologies are helping healthcare providers reduce hospitalization rates, improve treatment selection accuracy, and accelerate clinical decision-making. AI-enabled diagnostic platforms are also reducing diagnostic turnaround times significantly, improving patient outcomes while lowering operational costs for healthcare systems.

➡️ Become a valued research partner with us ☎ https://www.precedenceresearch.com/schedule-meeting

The Emerging Power of Transcriptomics in Personalized Care: Major Potential

The fast emergence of spatial and single-cell transcriptomics, driven by innovative platforms like Xenium, Molecular Cartography, and MERSCOPE, is revolutionizing biomedical research by redefining how we map disease etiology. These novel technologies bridge the gap between high-resolution cellular heterogeneity and precise tissue organization, providing a transformative opportunity to identify specific tissue biomarkers. This accelerates the development of targeted, next-generation therapeutics.

The convergence of artificial intelligence, bioinformatics, and next-generation sequencing is redefining precision medicine across oncology, infectious diseases, and rare genetic disorders. AI-powered pathology platforms are enabling faster image interpretation and biomarker detection, while machine learning algorithms are supporting predictive analytics for early disease identification. The growing use of companion diagnostics is further accelerating demand for highly personalized therapeutic strategies.

The Cost of Disjointed Regulations: Major Limitation

The adoption of advanced technologies like spatial transcriptomics is severely limited by a chaotic and fragmented global regulatory landscape, high compliance costs, and a lack of standardized protocols. This regulatory confusion, including stringent requirements under the EU In Vitro Diagnostic Regulation, restricts access to advanced instruments to well-funded institutions and delays the broader application of these technologies in clinical settings.

🔓 Instant Delivery Available | 💎 Buy Premium Report 👉 https://www.precedenceresearch.com/checkout/1130

Supply Chain Analysis – In Vitro Diagnostics Market

🔸Research and Development

This stage focuses on identifying novel biomarkers, developing assays, and

designing diagnostic instruments.

➢

Key

Players: Roche

Diagnostics, Abbott Laboratories, Thermo Fisher Scientific, Danaher

Corporation, bioMérieux, and QIAGEN.

🔸Regulatory Approval and

Clinical Validation

IVD products require strict validation of performance characteristics and

approval from regulatory bodies.

➢

Key

Players: Roche,

Abbott, Siemens Healthineers, Quest Diagnostics, and Bio-Rad Laboratories.

🔸Manufacturing

This stage involves high-volume, automated production of test kits, reagents,

and instruments to ensure reproducibility.

➢

Key

Players: Thermo

Fisher Scientific, Danaher, Bio-Rad Laboratories, Catalent, and Fujifilm

Diosynth Biotechnologies.

🔸Logistics and Distribution

Specialized logistics are required, including cold-chain management for

reagents and kits that need specific temperature storage to maintain integrity.

➢

Key Players: DHL Group, FedEx, Marken,

and UPS Healthcare.

In Vitro Diagnostics Market Report Scope

|

Report Coverage |

Details |

|

Market Size in 2025 |

USD 104.01 Billion |

|

Market Size in 2026 |

USD 106.16 Billion |

|

Market Size by 2035 |

USD 135.76 Billion |

|

Growth Rate (2026–2035) |

CAGR of 2.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2035 |

|

Segments Covered |

Product (Reagents, Instruments, Services), Technology (Immunoassay, Hematology, Clinical Chemistry, Molecular Diagnostics, Coagulation, Microbiology, Others), Application (Diabetes, Cardiology, Nephrology, Infectious Disease, Oncology, Drug Testing, Autoimmune Diseases, Others), Test Location (Point of Care, Home Care, Others), End User (Standalone Laboratories, Hospitals, Academic & Medical Schools, Point-of-Care, Others) |

|

Regional Scope |

North America, Europe, Asia-Pacific (APAC), Latin America, Middle East & Africa (MEA), Rest of the World |

|

Key Market Highlights |

→ North America captured

42% revenue share in 2025 |

|

Emerging Trends |

→ Growth of molecular

diagnostics and genomics/proteomics integration |

|

Market Drivers |

→ Rising demand for

precision medicine and decentralized diagnostics |

|

Market Challenges |

→ Regulatory complexity

and high infrastructure costs |

For questions or customization requests, please reach out to us @ sales@precedenceresearch.com | +1 804 441 9344

Driving Innovation in In Vitro Diagnostics: Real-World Success Stories

The In Vitro Diagnostics (IVD) market is not only growing in numbers but also transforming healthcare delivery worldwide. Recent initiatives demonstrate how advanced diagnostics are improving patient outcomes and accelerating precision medicine:

- Biocartis & Mayo Clinic Collaboration (Jan 2026): Together, they developed a rapid molecular test for breast cancer, significantly reducing the time needed to determine optimal treatment strategies. This case exemplifies how AI-driven diagnostics are enabling faster, personalized care.

- Sysmex India Plant Launch (Apr 2025): Sysmex operationalized its state-of-the-art facility to produce automated hematology analyzers locally. This expansion enhances supply reliability and ensures access to advanced diagnostics in emerging markets, supporting equitable healthcare.

- Roche SBX Sequencing Technology (Feb 2026): Roche introduced its Sequencing by Expansion (SBX) technology, offering ultra-rapid, high-throughput next-generation sequencing. The innovation underscores the role of cutting-edge molecular diagnostics in accelerating clinical decision-making.

- Home-Based PCR Testing (2025): Visby Medical’s FDA-approved 30-minute PCR test for STIs brings rapid, reliable diagnostics to patients’ homes, highlighting the trend toward decentralized, patient-centric testing solutions.

These examples showcase how technological innovation, AI integration, and global expansion are reshaping the diagnostics landscape, allowing faster, more precise, and patient-focused care.

Don’t Miss Out! | Instant Access to This Exclusive Report 👉 https://www.precedenceresearch.com/checkout/1130

In Vitro Diagnostics Market: Regional Analysis

North America dominated the IVD market in 2025, primarily due to its advanced healthcare infrastructure, high healthcare spending, and quick adoption of novel diagnostic technologies. A significant portion of the North American population suffers from chronic conditions such as diabetes, cardiovascular diseases, and cancer, necessitating frequent diagnostic testing and monitoring. Leading global IVD companies, including Abbott Laboratories, F. Hoffmann-La Roche, Thermo Fisher Scientific, BD, and Danaher Corporation, have a strong presence in the region, enhancing diagnostic precision.

As the undisputed global leader, the U.S. drives market innovation and is home to industry giants like Abbott and Thermo Fisher. The combination of personalized medicine, advancements in AI and NGS, and rapid point-of-care adoption, alongside a supportive regulatory environment from agencies like the FDA and CLIA, ensures robust technological integration into healthcare.

U.S. In Vitro Diagnostics Market Size, Trends, and Growth Forecast

According to Precedence Research, the U.S. in vitro diagnostics (IVD) market surpassed USD 35.43 billion in 2025 and is expected to reach USD 43.49 billion by 2035, at a CAGR of 2.07% from 2026 to 2035. The market growth is being driven by the rising adoption of precision medicine, increasing demand for molecular and point-of-care diagnostics, and continuous advancements in AI-enabled diagnostic technologies across healthcare systems.

U.S. In Vitro Diagnostics Market: Key Insights

- Market Overview: The U.S. in vitro diagnostics market is poised for strong growth, with a valuation of USD 35.43 billion in 2025, projected to reach USD 43.49 billion by 2035, reflecting an impressive CAGR of 207% from 2026 to 2035.

- By Product: Reagents dominate the market, commanding a 67% share in 2025, highlighting their critical role in diagnostic testing.

- By Test Location: Point-of-care testing leads the landscape, underscoring the shift toward faster, decentralized diagnostics for enhanced patient outcomes.

- By Technology: Immunoassays are expected to remain the technology of choice throughout the forecast period, driven by their high sensitivity and widespread applicability.

- By Application:

- Infectious diseases currently hold the largest market share, reflecting ongoing public health priorities.

- Oncology diagnostics are projected to witness the fastest growth, driven by rising cancer prevalence and the push for early detection solutions.

- By End User: Hospitals remain the primary end users, leveraging IVD solutions for routine and critical diagnostics.

- Market Trend: The market is increasingly characterized by rapid innovation, expansion of point-of-care platforms, and rising demand for personalized medicine, positioning the U.S. as a global leader in advanced diagnostic testing.

🔸In January 2026, Biocartis announced a collaboration with Mayo Clinic to develop a rapid sample-to-answer molecular diagnostics test for breast cancer, aiming to reduce the time needed to determine optimal treatment options.

This Report is Readily Available for Immediate Delivery | Download the Sample Pages of this Report@ https://www.precedenceresearch.com/sample/3712

The Canadian market is experiencing steady growth, driven by government modernization and a single-payer healthcare system, with a significant shift toward molecular, digital, and home-based diagnostics. While Canada relies heavily on imports for most medical devices, public laboratories facilitate the rapid and widespread adoption of these technologies, especially for infectious disease detection.

Asia Pacific region, the fastest growth is anticipated during the forecast period. This growth is fueled by a high burden of disease, rapid development of healthcare infrastructure, and improved diagnostic accessibility. A rapidly increasing elderly population, particularly in Japan, China, and South Korea, is driving the demand for routine diagnostic screenings and specialized care for age-related conditions. Additionally, governments in emerging economies like India and China are investing significantly in upgrading laboratory infrastructure and expanding public-private lab networks, making advanced diagnostics accessible beyond major urban centers.

India is rapidly transforming into a global powerhouse by leveraging cost-competitive, high-quality manufacturing and attracting global sourcing partners. A major focus on molecular diagnostics and decentralised point-of-care testing, championed by home-grown innovators, is revolutionizing access to diagnostics for infectious diseases, cementing its role as a key player in global health innovation.

🔸In April 2025, Sysmex will fully operationalize its new state-of-the-art Indian plant, manufacturing XQ-Series automated hematology analyzers. This move boosts local production of advanced diagnostics, aiding in improving healthcare quality and supply reliability across India. (Source: https://www.sysmex-ap.com)

China is rapidly cementing its status as a global powerhouse, transitioning from a manufacturing hub to a technological innovator. Driven by strong policy support, the nation boasts a robust domestic CLIA sector pushing high-speed automation and AI-based diagnostics. Backed by state funding for research and development, producing advanced, integrated systems, positioning as a global diagnostics landscape.

Global In Vitro Diagnostics Market Report Coverage

|

Market Scope |

Details |

|

Market Size in 2025 |

USD 104.01 Billion |

|

Market Size in 2026 |

USD 106.16 Billion |

|

Market Size in 2035 |

USD 135.76 Billion |

|

Market Growth Rate (2026–2035) |

CAGR of 2.7% |

|

Largest Regional Market |

North America |

|

Fastest Growing Region |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2035 |

|

Key Growth Driver |

Rising demand for precision medicine and decentralized diagnostics |

|

Key Market Opportunity |

AI-powered molecular diagnostics and home-based testing |

|

Major Market Challenge |

Regulatory complexity and high infrastructure costs |

|

Segments Covered |

By Product, By Technology, By Application, and region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

|

Key Companies Profiled |

Abbott Laboratories, Roche, Danaher, Bio-Rad, Sysmex, BD, Thermo Fisher Scientific |

|

Notable Industry Trend |

Expansion of AI-enabled point-of-care diagnostics |

|

Innovation Focus Areas |

Liquid biopsy, AI pathology, NGS, digital PCR, lab-on-a-chip technologies |

🔓 Instant Access. Zero Waiting. 📥 Buy the Premium Market Research Report Now 👉 https://www.precedenceresearch.com/checkout/1130

In Vitro Diagnostics Market Segmental Analysis

Product Type Analysis

The reagents segment dominated the market in 2025, driven by consistent high-volume demand for essential consumables that ensure accurate testing across all diagnostic platforms. The growing need for infectious disease testing and personalized medicine necessitates the continuous use of reagents in laboratories. These reagents are critical, proprietary components used across various modalities, including immunochemistry, molecular diagnostics, and clinical chemistry, which boosts the demand for small-scale reagent kits.

The instruments segment is expected to experience the fastest growth during the forecast period, primarily due to the increasing adoption of automated analyzers, point-of-care testing systems, and advanced molecular diagnostic platforms. The modernization of laboratories to enhance efficiency is leading to a higher adoption of fully automated analyzers, which provide better speed and accuracy. Hospitals are investing in advanced instrumentation to handle the rising volumes of high-complexity assays, particularly in molecular diagnostics and oncology.

Test Location Analysis

The point-of-care testing segment held the dominant position in the market in 2025, largely because of its ability to deliver rapid and accurate results outside traditional laboratory settings. Continuous advancements in automation and user-friendly platforms enable complex tests to be conducted in various locations. The evolution of molecular diagnostics from high-throughput laboratory tests to portable solutions is reducing turnaround times, driven by the growing demand for quick, actionable results for infectious diseases and cancer monitoring.

The home care segment is anticipated to grow the fastest during the forecast period, fueled by an increasing demand for convenience, privacy, and cost-effective chronic disease management. As patients move away from laboratory settings, there is a preference for home-based tests that provide immediate results for conditions such as diabetes and cardiovascular disease. Improved, user-friendly, and highly accurate rapid testing devices allow for reliable self-administered diagnostics and continuous monitoring, along with the availability of at-home tests for infectious diseases.

Technology Analysis

The molecular diagnostics segment dominated the market in 2025, primarily due to the rapid adoption of PCR, next-generation sequencing, and point-of-care molecular testing, all aimed at achieving high sensitivity, specificity, and faster turnaround times. Innovations in nanotechnology, microfluidics, and digital integration enable rapid, portable, and accurate molecular detection. The rise of at-home and point-of-care PCR diagnostics facilitates decentralized, quick results, expanding market penetration beyond laboratory settings and offering superior accuracy in detecting genetic and biochemical markers.

The immunoassay segment is projected to experience the fastest growth during the forecast period, driven by high-throughput automation, the increasing prevalence of chronic and infectious diseases, and the rapid adoption of point-of-care testing. Urine-based immunoassay testing is gaining popularity due to its non-invasive nature and wide applications, coupled with rising demand for rapid, high-sensitivity immunoassay-based point-of-care kits. The transition toward automated chemiluminescence immunoassays, known for their superior sensitivity and speed, is transforming clinical laboratories.

Faster diagnostics are transforming patient care. Early detection of cancer and rapid identification of infectious diseases mean patients receive critical results in hours instead of days, allowing timely interventions and better treatment outcomes

Application Analysis

The infectious disease segment led the market in 2025. This leadership is due to the high-volume testing for pathogens such as COVID-19, HIV, and tuberculosis. The increasing global incidence of infectious diseases, including respiratory infections and drug-resistant pathogens, necessitates consistent large-scale screening and diagnostic monitoring. The integration of automation and molecular diagnostics allows for faster processing of large sample volumes, enhancing laboratory efficiency. Increased funding for research and surveillance, with mandatory testing policies for infectious diseases, drives expansion.

The oncology segment is expected to experience the fastest growth during the forecast period, mainly due to the heightened demand for early cancer detection, the rise of personalized medicine, and the increased adoption of molecular diagnostics and non-invasive testing techniques. The shift toward tailored cancer therapies is generating demand for companion diagnostics to identify patients who would benefit from specific, targeted treatments. Additionally, minimally invasive liquid biopsies for cancer monitoring and relapse detection are poised to become major components of the market.

End User Analysis

The standalone laboratories segment dominated the market in 2025. This dominance is mainly driven by leveraging high-volume testing capabilities, adopting advanced automation, and offering extensive test menus. These laboratories, including major organized chains and independent labs, handle vast volumes of tests efficiently, often at a lower cost per test compared to hospitals. They utilize AI-integrated diagnostic tools and cutting-edge molecular diagnostics to provide faster, more accurate results. The integration of automated analyzers and workflow software allows for improving turnaround times.

The hospital segment is expected to have the fastest growth during the forecast period. This growth is mainly driven by high patient inflow, comprehensive testing needs, and the adoption of automated, high-throughput systems. Hospitals are adopting integrated automated laboratory systems to handle vast testing demands efficiently, strengthening their role in both routine and acute care. Increasing global rates of chronic diseases necessitate frequent, precise diagnostics, with hospitals acting as the primary hub for this testing, essential for inpatient care and emergency services.

✚ Related Topics You May Find Useful:

➡️ In Vitro Diagnostics Quality Controls Market: Explore how stricter regulatory standards and laboratory accuracy requirements are strengthening demand for advanced quality control solutions

➡️ Infectious Disease In Vitro Diagnostics Market: Discover how rising disease surveillance and rapid testing innovations are accelerating growth in infectious disease diagnostics

➡️ In Vitro Diagnostics Enzymes Market: Analyze the growing role of specialized enzymes in improving diagnostic precision, automation, and testing efficiency

➡️ PCR Based Transplant Diagnostics Market: Understand how PCR technologies are enhancing transplant compatibility testing and post-transplant monitoring outcomes

➡️ HIV Diagnostics Market: See how advancements in rapid screening and early detection technologies are reshaping global HIV testing strategies

➡️ Tissue Diagnostics Market: Track the increasing adoption of precision pathology tools and biomarker-based testing in cancer diagnostics

➡️ Infectious Disease Diagnostics Market: Gain insight into how evolving healthcare preparedness and molecular testing are transforming infectious disease detection worldwide

In Vitro Diagnostics Market Companies

➢ Alere, Inc.

➢ Hoffmann-La Roche Ltd.

➢ Arkray

➢ Beckman Coulter

➢ Becton Dickinson

➢ Bio-Rad Laboratories

➢ Danaher

➢ Sysmex Corporation

➢ Abbott Laboratories

Leading players are actively forming partnerships to innovate rapidly. Biocartis’ collaboration with Mayo Clinic on rapid breast cancer diagnostics and Sysmex’s Indian expansion exemplify efforts to enhance technology access and supply chains, strengthening the U.S. IVD ecosystem.

Key Emerging Innovations in the In Vitro Diagnostics Market

|

Innovation |

Description |

Recent Updates |

|

Liquid Biopsy/Multi-Omics |

Non-invasive detection of disease (mostly cancer) markers (ctDNA, CTCs) in blood/bodily fluids. |

GRAIL announced expansion of Galleri test applications; Guardant360 Liquid improved bioinformatic filtering. |

|

AI-Driven Diagnostics |

AI/ML algorithms to analyze imaging, genomics, and lab data for faster, accurate diagnosis. |

AI moved from support to partner; Pearl/VideaHealth achieved up to 89% sensitivity in AI-assisted systems. |

|

POC Molecular Testing |

Rapid, portable, cartridge-based nucleic acid testing (PCR/LAMP) near patient care. |

FDA approved Visby Medical’s no-prescription, 30-min home PCR test for STIs in 2025. |

|

Lab-on-a-Chip (LOAC) |

Miniaturized microfluidic systems integrating sample prep to result on one chip. |

Qiagen announced three automated, high-throughput sample prep instruments (QIAsymphony/Sprint) targeting 2026 launch. |

|

Next-Gen Sequencing (NGS) |

High-throughput sequencing for genetic profiling and personalized treatment. |

Illumina launched the MiSeq i100 benchtop series for on-demand sequencing; Roche targeted 2026 for SBX-based Axelios. |

You can place an order or ask any questions, please feel free to contact at sales@precedenceresearch.com | +1 804 441 9344

Major Shifts in the In Vitro Diagnostics Market

🔸In February 2026, Roche introduced its breakthrough sequencing by expansion (SBX) technology, a new category of next-generation sequencing. SBX chemistry and an innovative sensor module provide ultra-rapid, high-throughput sequencing that is flexible and scalable. This approach effectively addresses signal-to-noise challenges, allowing versatile operation across various throughput scales, according to Mark Kokoris, Head of Roche's SBX Technology. (Source: https://www.roche.com)

🔸In February 2025, Bio-Rad Laboratories announced plans to acquire Stilla Technologies, which specializes in next-generation digital PCR instruments and assays. The acquisition aims to enhance Bio-Rad's digital PCR portfolio and expand its reach in applied research and clinical diagnostics. CEO Norman Schwartz stated the move would support high automation and throughput capabilities. (Source: https://investors.bio-rad.com)

🔸In February 2025, Revvity, Inc. launched three Mimix™ reference standards for IVD use, designed to monitor next-generation sequencing and ddPCR assays for somatic mutations in genomic DNA. These standards comply with FDA regulations to support lab workflows and help identify errors. The three Mimix reference standards focus on key cancer testing applications and are derived from human cell lines to maintain genomic complexity. (Source: https://news.revvity.com)

In Vitro Diagnostics Market Segmentation

By Product

🔸Reagents

🔸Instruments

🔸Services

By Test Location

🔸Point of Care

🔸Home Care

🔸Others

By Technology

🔸Immunoassay

→ Instruments

→ Reagents

→ Services

🔸Hematology

→ Instruments

→ Reagents

→ Services

Clinical Chemistry

→ Instruments

→ Reagents

→ Services

🔸Molecular Diagnostics

→ Instruments

→ Reagents

→ Services

🔸Coagulation

→ Instruments

→ Reagents

→ Services

🔸Microbiology

→ Instruments

→ Reagents

→ Services

🔸Others

→ Instruments

→ Reagents

→ Services

By Application

🔸Diabetes

🔸Cardiology

🔸Nephrology

🔸Infectious Disease

🔸Oncology

🔸Drug Testing

🔸Autoimmune Diseases

🔸Others

By End User

🔸Standalone Laboratories

🔸Hospitals

🔸Academic & Medical Schools

🔸Point-of-Care

🔸Others

By Region

🔸North America

🔸Europe

🔸Asia-Pacific

🔸Latin America

🔸The Middle East and Africa

Immediate Delivery Available | Buy This Premium Research Report@ https://www.precedenceresearch.com/checkout/1130

About Us

Precedence Research is a global market intelligence and consulting powerhouse, dedicated to unlocking deep strategic insights that drive innovation and transformation. With a laser focus on the dynamic world of life sciences, we specialize in decoding the complexities of cell and gene therapy, drug development, and oncology markets, helping our clients stay ahead in some of the most cutting-edge and high-stakes domains in healthcare. Our expertise spans across the biotech and pharmaceutical ecosystem, serving innovators, investors, and institutions that are redefining what’s possible in regenerative medicine, cancer care, precision therapeutics, and beyond.

Web: https://www.precedenceresearch.com

Our Trusted Data Partners:

Towards Healthcare | Nova One Advisor | Market Stats Insight

Connect With Us

📞 USA: +1 804 441 9344

📞 APAC: +61 485 981 310 or +91 87933 22019 | +6531051271

📞 Europe: +44 7383 092 044

📩 Email: sales@precedenceresearch.com

Get Recent News:

https://www.precedenceresearch.com/news

For the Latest Update Follow Us: