The generic drugs market is entering a transformative phase, driven by innovation and rising demand for affordable healthcare. Advances in biosimilars and AI-powered manufacturing are improving access and efficiency. With growing chronic diseases and patent expirations.

According to Precedence Research, the global generic drugs market size is expected to grow from USD 491.67 billion in 2026 to nearly USD 762.48 billion by 2035, with a CAGR of 5% over the next decade.

The industry is undergoing a structural transformation from high-volume, low-margin commoditized drugs to high-value, complex generics and biosimilars creating new opportunities for pharmaceutical companies, investors, and healthcare systems worldwide.

Across the globe, the generic drugs market is experiencing a significant transformation, shifting from commoditized small molecules to high-value, complex generics and biosimilars. This change is primarily driven by the expiration of patents for major biologics in oncology and chronic disease management. To mitigate pricing pressures and meet stringent FDA/EMA quality standards, manufacturers are accelerating the adoption of automated, continuous manufacturing and AI-driven bioequivalence modeling. These strategies aim to increase efficiency, shorten development cycles, and ensure long-term sustainability.

Where Data Meets Strategic Clarity 📥 View Sample Pages of the Complete

Report 👉https://www.precedenceresearch.com/sample/1205

Generic Drugs Market Highlights:

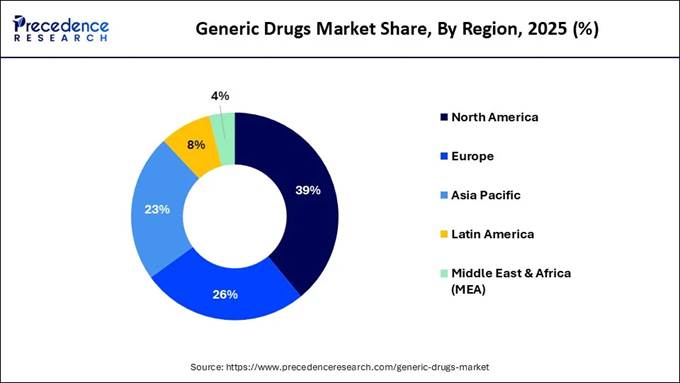

🔹North America dominated with the largest market share of 39% in 2025.

🔹Asia Pacific is anticipated to have the fastest growth with a notable CAGR during the forecast period.

🔹By drug type, the simple generics segment contributed the highest market share in 2025.

🔹By drug type, the super generics segment is growing at a strong CAGR between 2026 and 2035.

🔹By brand, the pure generic drug segment held a major market share in 2025.

🔹By brand, the branded generic drugs segment is expected to expand at a notable CAGR from 2026 to 2035.

🔹By route of drug administration, the oral segment captured the highest market share in 2025.

🔹By route of drug administration, the injection segment is poised to grow at a healthy CAGR between 2026 and 2035.

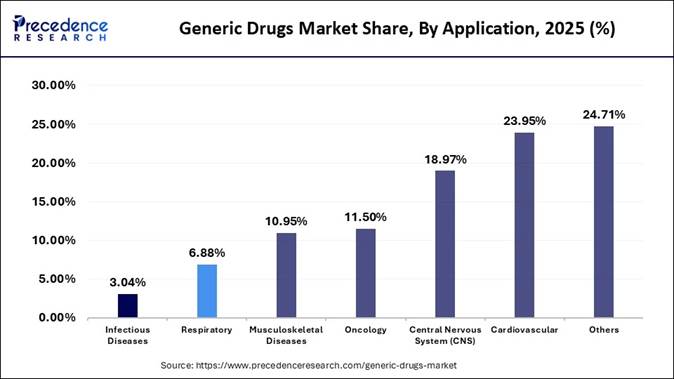

🔹By therapeutic application, the cardiovascular segment generated the biggest market share in 2025.

🔹By therapeutic application, the oncology segment is expanding at the fastest CAGR between 2026 and 2035.

🔹By distribution channel, the retail pharmacy segment accounted for the largest market share in 2025.

🔹By distribution channel, the hospital pharmacy segment is projected to grow at a solid CAGR between 2026 and 2035.

Market Overview: The Expanding Power of Generic Drugs

The generic drugs market, which comprises non-branded, affordable alternatives to brand-name medications that are chemically identical in active ingredients, dosage, strength, and route of administration, is expanding rapidly. This growth is fueled by the rising prevalence of chronic diseases, cost-containment measures, and a significant patent cliff affecting high-revenue drugs. These products offer identical therapeutic effects at a fraction of the cost and are increasingly dominating the pharmaceutical sector, with the Asia-Pacific region serving as a major manufacturing hub.

➡️ Become a Valued Research Partner with Us https://www.precedenceresearch.com/schedule-meeting

Investing in Complex Generics and Biosimilars: Major

Potential

The market

is shifting toward complex generics and biosimilars, largely driven by the

upcoming patent expirations of blockbuster biologics. This high-value segment

promises higher profit margins due to increased technical and regulatory

barriers. With advancements in AI-driven modeling and drug delivery, the

biosimilar market is projected to expand significantly - especially in oncology

and autoimmune therapies. Pharmaceutical firms are focusing on these areas to

ensure long-term, sustainable growth. The High

Cost of Narrow Sourcing: Major Limitations The generic

drugs market faces substantial limitations due to intense competition, which

causes severe price erosion, often dropping below production costs upon market

entry. This scenario, combined with high capital expenditures for research and

development and quality compliance, heavily compresses profit margins and leads

to industry consolidation. Additionally, this economic pressure results in

strategic vulnerabilities, creating significant supply chain risks in the event

of regional disruptions. 🔗 Stay Ahead of the Market

Curve — Get the Full Report 👉 https://www.precedenceresearch.com/generic-drugs-market Generic

Drugs Market Leading Companies ➢ Mylan N.V. ➢ Abbott

Laboratories ➢ ALLERGAN ➢ Teva

Pharmaceutical Industries Ltd. ➢ Eli Lilly and

Company ➢ STADA

Arzneimittel AG ➢ GlaxoSmithKline

Plc. ➢ Baxter

International Inc. ➢ Pfizer Inc. ➢ Sandoz

International GmbH Value

Chain Analysis: Generic Drugs Market The generic

drugs market operates through a multi-stage value chain, encompassing research

and development, distribution, and patient-centric services. Each stage

involves specialized processes and key industry participants. Research

& Development (R&D) 🔸This initial stage focuses on

strategic planning and candidate selection, followed by pharmaceutical

development and bioequivalence studies. It also includes clinical evaluations,

scale-up processes, manufacturing readiness, and regulatory submission and

review. 🔸Key companies driving this segment

include Sandoz, Sun Pharma, Fosun Pharma, Viatris, Aurobindo Pharma, Teva

Pharmaceuticals, Cipla, and Lupin. Distribution

to Hospitals and Pharmacies 🔸This stage encompasses the core

supply chain operations, including the transfer of products from manufacturers

to distributors, warehousing, order management, and last-mile delivery to

hospitals and retail pharmacies. 🔸Major participants in this segment

include McKesson Corporation, Cencora, Cardinal Health, along with

manufacturers such as Sandoz, Teva Pharmaceuticals, Viatris, Sun Pharma, and

Fosun Pharma. Patient

Support & Services 🔸The final stage focuses on enhancing

patient outcomes through support programs. This includes patient enrollment,

awareness initiatives, access and affordability programs, therapy initiation,

education, adherence monitoring, and long-term treatment maintenance. 🔸Key organizations operating in this

space include Fortrea, AssistRx, CareMetx LLC, ConnectiveRx, Lash Group,

McKesson Corporation, Cardinal Health, EVERSANA, and United BioSource LLC. Generic

Drugs Market Report Coverage Report Coverage Details Market Size in 2025 USD 468.08 Billion Market Size in 2026 USD 491.67 Billion Market Size by 2035 USD 762.48 Billion Market CAGR (2026–2035) CAGR of 5% Largest Market North America Fastest Growing Region Asia-Pacific Base Year 2025 Forecast Period 2026 to 2035 Segments Covered Drug, Brand, Route of Drug

Administration, Therapeutic Application, Distribution Channel and Regions Regions Covered North America, Europe, Asia-Pacific,

Latin America, Middle East & Africa Key Growth Drivers Rising chronic diseases,

patent expirations, and strong demand for low-cost alternatives are driving

generic drug adoption globally. Key Technology Trends AI-based modeling, continuous

manufacturing, and advances in complex generics and biosimilars are improving

efficiency and innovation. Major Opportunity Biosimilars and complex

generics offer high-margin growth, supported by biologics patent expirations

and emerging market demand. Key Challenge Severe price erosion, API

dependency, and strict regulatory requirements continue to pressure margins

and delay approvals. Leading Market Participants Teva Pharmaceutical

Industries Ltd., Pfizer Inc., Sandoz International GmbH, Abbott Laboratories,

and Mylan N.V.

Have questions or ready to move forward? Contact our experts

today @ sales@precedenceresearch.com | +1 804

441 9344 Generic Drugs

Market: Regional Analysis North America

dominated the market in 2025, primarily due to high healthcare expenditure, an aging

population, and a regulatory environment that prioritizes cost-effective,

high-quality alternatives to branded drugs. The high prevalence of chronic

conditions, such as diabetes, hypertension, and cardiovascular diseases,

necessitates long-term medication, driving demand for affordable, sustainable

treatment options. High drug costs put immense pressure on payers to promote

cheaper alternatives, while the patent cliff ensures a continuous pipeline of

new generic products. As the

world's largest generic drug market, the U.S. dominates prescriptions filled

by generics, driven by high demand from an aging population and cost-saving

initiatives. Regulated by the FDA's OGD to ensure quality, the market is

shifting toward complex generics, biosimilars, and automated manufacturing to

meet the growing need for affordable treatments. Get informed with deep-dive intelligence on AI’s market

impact 👉 https://www.precedenceresearch.com/ai-precedence U.S.

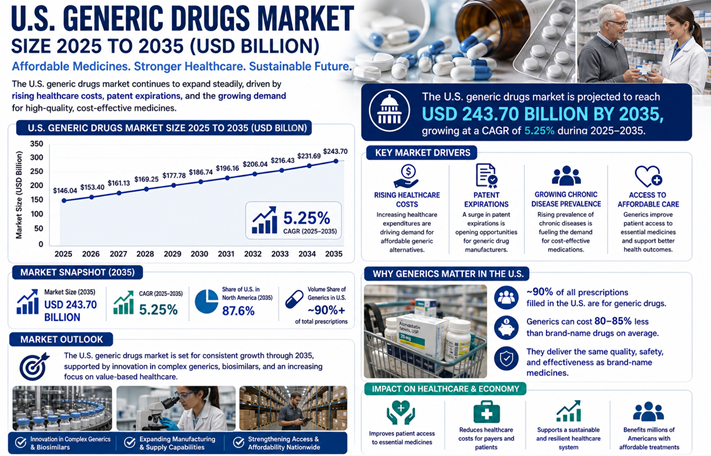

Generic Drugs Market Size and Growth 2025 to 2035 The U.S. generic drugs market size is expected to touch USD 243.70

billion by 2035 increasing from USD 153.40 billion in 2026, The market is

poised to grow at a CAGR of 5.25% between 2026 and 2035. The U.S.

Generic Drugs Market Report is Readily Available 📥 Download Sample Pages of the Report 👉 https://www.precedenceresearch.com/us-generic-drug-market Report Coverage Details Market Size in 2025 USD 146.04 Billion Market Size in 2026 USD 153.40 Billion Market Size by 2035 USD 243.70 Billion Growth Rate (2026–2035) CAGR of 5.25% Base Year 2025 Forecast Period 2026 to 2035 Segments Covered By Drug Type, By Brand,

By Route of Administration, By Therapeutic Application, By Distribution

Channel Market Position Largest global generic

drugs market with strong FDA regulatory framework Prescription Share Generics account for 90%+

of total prescriptions in the U.S. Cost Advantage Generics are 80–85%

lower in cost compared to branded drugs Key Growth Drivers Patent expirations,

rising chronic diseases, aging population, demand for affordable therapies Innovation Trends Growth in biosimilars,

complex generics, AI-driven drug development, and continuous manufacturing Regulatory Landscape Strong support through

FDA initiatives such as GDUFA III enhancing approvals and innovation Healthcare Impact Improves accessibility,

reduces healthcare costs, and supports sustainable healthcare systems

Leading

Players Shaping the U.S. Generic Drugs Market The U.S.

generic drugs market is driven by a combination of global pharmaceutical

leaders and cost-efficient manufacturers, focusing on affordability,

innovation, and supply reliability. 🔹 Key Market Participants ➢ Pfizer Inc.: Focuses on hospital-based

generics, particularly sterile injectables and anti-infectives. Its strong

domestic manufacturing network supports consistent supply and high-quality

standards. ➢ Teva Pharmaceuticals USA Inc.: A leading generics

provider with a broad portfolio across CNS, oncology, and cardiovascular

therapies. Increasingly focused on complex generics and specialty medicines. ➢ Aurobindo Pharma USA Inc.: Specializes in high-volume

oral solids and injectable generics. Its vertically integrated model enables

cost efficiency and competitive pricing. Other Major Key Players ➢ Sun Pharma Inc.: Expanding its U.S.

presence with a diversified generics and specialty portfolio. ➢ Abbott Laboratories Inc.: Maintains a strong

position through global reach and trusted healthcare solutions. ➢ Lupin Pharmaceuticals, Inc.: Focused on respiratory and

cardiovascular segments, with growing investments in complex generics. ➢ Mylan (Viatris): A major supplier of

affordable medicines, offering a wide and diversified generics portfolio. ➢ Dr. Reddy’s Laboratories: Strengthening its

footprint through biosimilars and advanced generic formulations. ➢ Novartis (Sandoz Division): A global leader in biosimilars

and complex generics, driving innovation in high-value segments. ➢ Eli Lilly and Company: Expanding into generics

and biosimilars through strategic partnerships and product development

initiatives. 🔓 Instant Access. Zero Waiting. 📥 Buy the Premium Market

Research Report Now 👉 https://www.precedenceresearch.com/checkout/2486 U.S. Generic Drugs Market Segments Covered in the Report By Drug Type • Simple Generics • Super Generics By Brand • Pure Generic Drugs • Branded Generic Drugs By Route of Administration • Oral • Injection • Cutaneous • Others By Therapeutic Application • Central Nervous System (CNS) • Cardiovascular • Infectious Diseases • Musculoskeletal Diseases • Respiratory • Oncology • Others By Distribution Channels • Retail Pharmacy • Hospital Pharmacy • Online and Others Browse Our Subscription Plans@ https://www.precedenceresearch.com/get-a-subscription Canada

holds a significant position in the generic drug market, characterized by high utilization

rates and a robust regulatory framework under Health Canada that ensures safety

and cost management. The sector leverages a strong manufacturing footprint and

an aggressive shift toward biosimilars to secure savings for complex

treatments. As the

world's largest provider of generic drugs, India holds a dominant global

position by supplying export volume and boasting the highest number of U.S.

FDA-approved manufacturing sites. Renowned for affordable, high-quality

medications, particularly in vaccines, cardiovascular, and antibiotic segments, the industry is critical

to global health security, as India remains heavily dependent on China for

approximately two-thirds of its APIs and key starting materials. 🔸 In March 206, the Production Linked Incentive

(PLI) Scheme is a strategic initiative aimed at reducing import reliance on

China by offering financial incentives to boost domestic manufacturing of APIs,

Key Starting Materials, and drug intermediates. (Source: https://www.pib.gov) As the

world’s leading manufacturer and exporter of APIs, China dominates the global

generic drug supply chain by providing the vast majority of critical ingredients

for essential medicines. While maintaining unmatched cost efficiency and scale,

China is aggressively shifting its market strategy to move up the value chain

by rapidly upgrading quality standards, strengthening regulatory compliance in

advanced manufacturing and biotech technologies.

Generic Drugs Market: Segmentation Analysis

By Drug Type Analysis

The simple generics segment dominated the market in

2025, largely due to high demand for

affordable treatments, widespread patent expirations on blockbuster drugs, and

established manufacturing pipelines. These generics provide the same therapeutic

effects as branded drugs but at a significantly lower cost, driving their

adoption among patients and healthcare systems aiming to control spending. The

rising prevalence of chronic conditions ensures a consistent, high-volume

demand for these often oral medications.

The super generics segment is expected to witness the

fastest growth during the forecast period. This growth is primarily driven by the intense demand for improved

patient compliance and enhanced bioavailability. Also known as value-added generics,

super generics often enhance the original drug's formulation, such as improving

its absorption rate, making them superior to standard generics. The growing

number of brand-name drug patents expiring, combined with the rising prevalence

of chronic conditions, is driving demand for these superior alternatives.

By Brand

Analysis The pure

generic drug segment led the market in 2025, primarily driven by affordability and bioequivalence

to branded counterparts. Pure generics, which do not have a brand name and

typically use the generic name, are preferred for controlling healthcare costs.

The expiration of brand-name patents creates significant market opportunities,

allowing for the rapid adoption of affordable alternatives. There is also high demand

for low-cost, effective medication in emerging economies, further enhancing the

market share of pure generic products. The

branded generic drugs segment is expected to experience the fastest growth

during the forecast period. This growth is fueled by the increasing demand for cost-effective

alternatives to branded drugs, the rising burden of chronic diseases, and

improved regulatory approval rates. Patients and healthcare providers prefer

lower-cost branded alternatives, which boosts demand. Branded generics offer

familiar names, fostering greater trust and loyalty among consumers, while the

patent cliff enables many high-revenue branded drugs to transition to generic

manufacturing. By Route

of Drug Administration Analysis The oral

segment accounted for the largest market share in 2025. This is largely due to the

unparalleled convenience, cost-effectiveness, and high patient adherence

associated with oral tablets, capsules, and liquids. Oral medications are

non-invasive and easy to self-administer, making them preferable for patients,

especially those managing chronic diseases that require long-term, daily

medication. Additionally, oral solid dosage forms such as tablets and capsules

are generally easier and cheaper to manufacture, store, and transport, contributing

to lower pricing. The

injection segment is projected to experience the fastest growth during the

forecast period.

This growth is mainly driven by the increasing demand for biosimilars, complex

generics, and therapies for chronic diseases that require high bioavailability.

There is substantial demand for injectable medications in the treatment of

cancer, diabetes, and autoimmune disorders, driving adoption. Injections

provide an immediate onset of action and are ideal for drugs that are poorly absorbed

when taken orally, ensuring 100% bioavailability in many cases, which allows

for the rapid rise of cheaper injectable alternatives. By

Therapeutic Application Analysis The

cardiovascular segment led the market in 2025, primarily due to the high prevalence rates of

chronic conditions such as hypertension and high cholesterol, which ensure

sustained long-term demand. Cardiovascular diseases are a leading cause of

mortality worldwide, necessitating ongoing medication use and ensuring a steady

revenue stream. The generic cardiovascular segment benefits from the loss of

patent protection for numerous blockbuster drugs, facilitating the rapid

introduction of cheaper, bioequivalent alternatives. The oncology

segment is experiencing the fastest growth during the forecast period, primarily due to the high

prevalence of cancer and the expiration of patents on blockbuster drugs.

Cost-effective, high-quality generic alternatives are replacing expensive

brand-name drugs, driving demand. Additionally, the increasing adoption of

targeted therapies and biosimilars further accelerates market growth. The

introduction of biosimilars, generic alternatives for complex biologic drugs, is

transforming the market and encouraging the adoption of generic drugs. By Distribution

Channel Analysis The

retail pharmacy segment dominated the market in 2025, primarily due to its ability to

provide convenient access to affordable, daily-use medications for chronic

diseases. The widespread availability of retail pharmacies, along with trusted

counseling services and high consumer foot traffic, facilitates quick access to

and fulfillment of prescriptions. Retailers often offer competitive pricing and

discounts on generic drugs, making them the primary channel for lower-cost trade

generics, which helps consumers manage their healthcare costs. The

hospital pharmacy segment is expected to witness the fastest growth during the

forecast period.

This growth is driven by increasing hospital admissions, rising demand for

inpatient care, and the consolidation of purchasing power through institutional

group purchasing organizations. Hospital pharmacies play a crucial role in the

growing use of specialty generics, including oncology and parenteral drugs for

complex therapies in acute care settings. The rising number of hospital

admissions and the need for immediate access to treatments necessitate a strong

reliance on hospital pharmacies. ✚ Related

Topics You May Find Useful: ➡️ Inhalation and Nasal

Spray Generic Drugs Market: Explore how respiratory therapies and convenient drug delivery

formats are shaping generic drug adoption ➡️ Antibody Drug

Conjugates Market:

Discover advancements in targeted cancer therapies combining precision

biologics with potent cytotoxic agents ➡️ Chemical Drug CDMO

Market: Understand the

growing role of outsourcing in drug development and manufacturing efficiency ➡️ Transdermal Drug

Delivery Systems Market:

Analyze the shift toward non-invasive delivery methods improving patient

compliance ➡️ Nasal Drug Delivery

Technology Market:

Examine innovations enabling rapid absorption and enhanced therapeutic

effectiveness ➡️ Drug Discovery

Informatics Market:

See how data-driven technologies and AI are transforming pharmaceutical

research processes ➡️ Antipsychotic Drugs

Market: Gain insight

into treatment advancements addressing mental health disorders worldwide ➡️ Genitourinary Drugs

Market: Track evolving

therapies targeting urinary and reproductive health conditions Emerging Innovation Description and Focus Area Application Area 3D Printing for Personalised Dosages On-demand manufacturing and patient compliance.

Allows precise dosing, customized shapes, and rapid-dissolving forms for

special populations. Spritam (levetiracetam): 3D printed for rapid

dissolution; FabRx oral thin films for personalized doses. Continuous Manufacturing (CM) Quality and efficiency. Replaces batch processes

with seamless, automated flow, enhancing quality assurance (QbD) and lowering

costs. Small molecule tablets: CM is used to cut production

times by up to 50% for high-volume generic drugs. Nanotechnology in Drug Delivery Bioavailability and targeting. Encapsulating APIs in

nano-carriers improves solubility and targeted delivery, specifically for

poorly soluble drugs. Abraxane (paclitaxel): Albumin-bound nanoparticle

formulation; SUBACAP (itraconazole) for enhanced solubility. AI-Driven Bioequivalence (BE) Modeling Regulatory approval speed. AI/ML algorithms analyze

datasets to simulate pharmacokinetic studies, reducing the need for costly

human trials. FDA BEAM Tool: Bioequivalence Assessment Mate to

automate and accelerate ANDA approvals. Biosimilars and Complex Generic Development Access to high-value biologics. Developing generic

alternatives to complex biologics facing patent cliffs in oncology and

immunology. Stelara (Ustekinumab) biosimilars: Targeted for

launch following patent expiration.

Major

Shifts in the Generic Drugs Market 🔸In March 2026, the first wave of generic versions

of Novo Nordisk’s GLP-1 weight-loss drugs launched in India, with domestic

drugmakers cutting prices by up to 80% after the patent expired. This is

crucial, with around 100 million people living with diabetes and a significant

obesity rate and aims to be among the top players in this space. (Source: https://www.cnbc.com) 🔸In March 2026, Hyderabad-based pharma major Dr

Reddy’s Laboratories (DRL) has launched its semaglutide generic, Obeda, for

Type 2 diabetes management in India. The launch comes a day after semaglutide

lost its patent protection. The cost to the patient for Obeda is ₹4,200 per

month for its 2 milligram (mg) and 4 mg versions- a 62 per cent drop from the

highest dosage form of the innovator drug Ozempic. (Source: https://www.business-standard.com)

🔸 In January 2026, Dr. Reddy’s also announced the U.S.

launch of olopatadine hydrochloride (HCl) ophthalmic solution, a generic

version of Alcon’s Pataday, marking its first-to-market launch. It is an

over-the-counter eye drop for allergy relief approved for use in adults and

children aged 2 and above. (Source: https://glance.eyesoneyecare.com) Generic

Drugs Market Segmentation By Drug

Type 🔹Simple Generics 🔹Super Generics By Brand 🔹Pure generic drugs 🔹Branded generic drugs By Route

of Drug Administration 🔹Oral 🔹Injection 🔹Cutaneous 🔹Others By

Therapeutic Application 🔹Central Nervous System (CNS) 🔹Cardiovascular 🔹Infectious Diseases 🔹Musculoskeletal Diseases 🔹Respiratory 🔹Oncology 🔹Others By

Distribution Channel 🔹Retail Pharmacy 🔹Hospital Pharmacy 🔹Online and Others By Region 🔹North America 🔹Asia Pacific 🔹Europe 🔹Latin America 🔹Middle East and Africa (MEA) Thanks for reading you can also get individual

chapter-wise sections or region-wise report versions such as North America,

Europe, or Asia Pacific. Don’t Miss Out! | Instant Access to This

Exclusive Report 👉 https://www.precedenceresearch.com/checkout/1205 You can place an order or ask any questions, please feel free

to contact at sales@precedenceresearch.com | +1 804 441 9344 Stay Ahead with Precedence Research Subscriptions Unlock

exclusive access to powerful market intelligence, real-time data, and

forward-looking insights, tailored to your business. From trend tracking to competitive

analysis, our subscription plans keep you informed, agile, and ahead of the

curve. Browse

Our Subscription Plans@ https://www.precedenceresearch.com/get-a-subscription About Us Precedence

Research is a global market intelligence and consulting powerhouse, dedicated

to unlocking deep strategic insights that drive innovation and transformation.

With a laser focus on the dynamic world of

life sciences,

we specialize in decoding the complexities of cell and

gene therapy,

drug development, and oncology markets, helping our clients stay ahead in

some of the most cutting-edge and high-stakes domains in healthcare. Our

expertise spans across the biotech and pharmaceutical ecosystem, serving

innovators, investors, and institutions that are redefining what’s possible in regenerative medicine, cancer care, precision

therapeutics, and beyond. Web: https://www.precedenceresearch.com Our

Trusted Data Partners: Towards Healthcare | Nova One Advisor | Statifacts Get

Recent News 👉 https://www.precedenceresearch.com/news For

Latest Update Follow Us:

🔸 In

January 2026, GDUFA

Regulatory Science Initiatives under GDUFA III are prioritizing the integration

of AI, machine learning, and advanced manufacturing

technologies to modernize generic drug development and assessment, aiming to

enhance efficiency and facilitate the development of complex generic medicines.

(Source: https://www.fda.gov)

U.S. Generic Drugs Market Scope and Key Insights:

Asia-Pacific region is anticipated to experience the fastest growth during the

forecast period. This growth is driven by a massive population, an increasing

burden of chronic diseases, significant government initiatives to reduce

healthcare costs, and a strong local manufacturing base. Governments are advocating

for affordable treatments to minimize overall health spending, especially given

the high prevalence of chronic illnesses requiring long-term therapies. India

and China are emerging as global hubs for generic drug manufacturing, offering

competitive pricing due to skilled labor and established supply chains.

Emerging innovations in the Generic Drugs