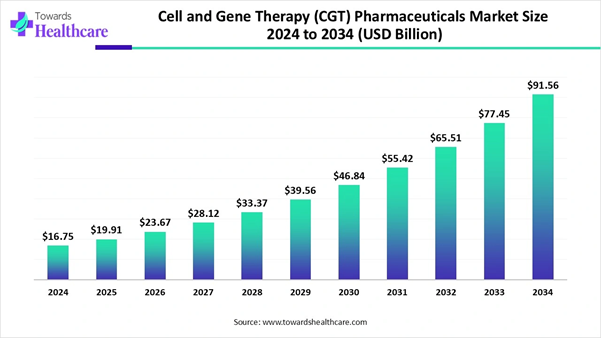

Market insights predict, the cell and gene therapy (CGT) pharmaceuticals market is expected to grow from USD 16.75 billion in 2024 to USD 91.56 billion by 2034, driven by a CAGR of 18.93%. The growing demand for personalized medicine, driving patient-specific therapies, is estimated to drive the growth of the market. North America led the global market owing to a strong clinical trial landscape, as the U.S. hosts the majority of global trials in cell and gene therapy.

The Complete Study is Now Available for Immediate Access | Download the Sample Pages of this Report @ https://www.towardshealthcare.com/download-sample/6099

Key Takeaways

➜ Cell and gene therapy (CGT) pharmaceuticals market to crossed USD 16.75 billion by 2024.

➜ Market projected at USD 91.56 billion by 2034.

➜ CAGR of 18.93% expected in between 2025 to 2034.

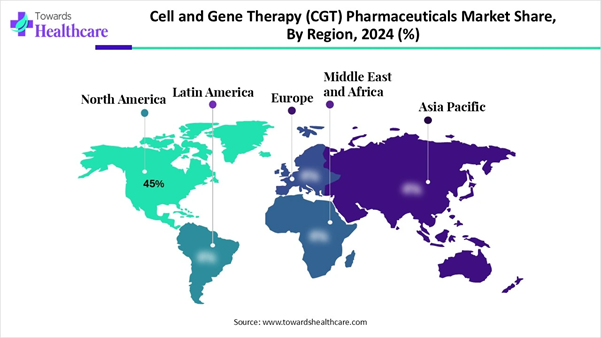

➜ North America held a major revenue share of approximately 45% in the market in 2024.

➜ Asia-Pacific is expected to witness the fastest growth during the predicted timeframe.

➜ By therapy type, the cell therapies segment registered its dominance over the global market with a share of approximately 45% in 2024.

➜ By therapy type, the gene editing & gene modulation segment is expected to grow with the highest CAGR in the market during the studied years.

➜ By modality/vector & delivery platform, the viral vectors segment held a dominant presence in the cell and gene therapy (CGT) pharmaceuticals market with a share of approximately 52% in 2024.

➜ By modality/vector & delivery platform, the non-viral delivery segment is expected to witness the fastest growth in the market over the forecast period.

➜ By route of administration, the intravenous/systemic infusion segment contributed the biggest revenue share of approximately 50% in the market in 2024.

➜ By route of administration, the intrathecal/intracerebral/CNS direct delivery segment is expected to grow at the fastest CAGR in the market during the forecast period.

➜ By manufacturing & supply model, the in-house manufacturing by sponsors segment accounted for a maximum revenue share of approximately 55% in the market in 2024.

➜ By manufacturing & supply model, the outsourced & CDMO manufacturing segment is expected to expand rapidly in the cell and gene therapy (CGT) pharmaceuticals market in the coming years.

➜ By end user /customer, the hospitals & specialized infusion centers segment contributed the biggest revenue share of approximately 60% in the market in 2024.

➜ By end user/customer, the CDMOs & contract labs segment is expected to grow at the fastest CAGR in the market during the forecast period.

What is Cell and Gene Therapy (CGT) Pharmaceuticals Market?

The pharmaceuticals market for gene therapies and cell therapies is currently experiencing the start of a huge industry overhaul. Recent advances in gene therapy and cell therapy have moved it away from the research and development stage towards the treatment stage. The healthcare community is increasingly embracing gene therapies that have the potential to cure disease at their genetic roots instead of just managing the symptoms associated with them. There is an intense race between the companies to increase the volume of products they can produce and manufacture, to make the regulatory processes to receive approval from organizations such as the FDA faster and easier, and to establish as many new potential therapies in the clinical pipeline as possible.

Investors are currently pouring money into this area because of the new and incredible opportunity these types of therapies provide as the potential to provide long-term cures and personalized medicine. As new delivery systems, vector engineering and off-the-shelf therapies continue to evolve and develop, the industry is continuing to change, with a significant amount of innovation continuing to be introduced. The industry is on the cusp of becoming a major segment of advanced medicine, potentially permanently changing the way some of the most complex diseases in the world are treated.

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

What Forces Are Powering the Cell and Gene Therapy Pharmaceuticals Market?

Consistent with our previous paragraphs analyzing market drivers, we note that support for development and use of next-generation therapeutic solutions by regulatory agencies and the continued increase in prevalence of rare genetic disorders and complex chronic diseases will create an environment conducive to rapid growth and innovation in the industry. As a result, the combination of these positive market dynamics resulting from the increased use of these types of therapies, the proliferation and enhancement of technology being developed, and the greater support from government to get treatments to market has created momentum for us to see unprecedented growth and innovation in our industry over the next few years.

How Can AI Improve the Cell and Gene Therapy (CGT) Pharmaceuticals Market?

AI integration can significantly enhance the market by accelerating research, development, and commercialization processes. In drug discovery, AI algorithms can analyze massive datasets to identify novel therapeutic targets and optimize gene-editing techniques with higher precision. During clinical trials, AI can streamline patient recruitment, predict treatment responses, and monitor safety outcomes in real time, reducing costs and timelines. In manufacturing, AI-driven automation ensures consistency, scalability, and quality control of complex cell-based products.

Moreover, AI supports personalized medicine by analyzing genomic and patient data to tailor therapies for maximum efficacy. It also improves regulatory compliance through predictive analytics and documentation automation. By enabling faster innovation, cost efficiency, and precision, AI integration addresses key challenges such as high development costs, long approval cycles, and scalability issues, thereby driving broader accessibility and adoption of cell and gene therapies in the global pharmaceuticals market.

What Problems Are Remaining to Be Resolved for the Gene and Cell Therapies Drug Industry?

The gene and cell therapies industry is growing but, has significant challenges due to the complexity of the production process. The slow and expensive nature of cell and gene therapies is causing most therapies to face significant logistical issues, such as cold-chain requirements, limited vector production capacity, and highly specialised production processes. The regulatory landscape continues to evolve and introduce uncertainty for manufacturers who want to innovate while complying with regulations. In addition, there is a lack of access for patients with limited financial resources, and the cost of treatment is creating a financial burden on healthcare providers in their reimbursement processes.

Manufacturers must also work to increase safety and efficacy by conducting studies to learn more about the long-term impact of their cellular and gene therapy products on patients, including immunological responses, long-term side effects and potentially unintended genetic changes. Given the complexity of the relationship between science, economics and operations, therefore, the growth of the gene and cell therapies market will not increase until these scientific, economic and operational challenges are adequately addressed.

Regional Insight

Why Does North America Dominates the Cell and Gene Therapy (CGT) Pharmaceuticals Market?

North America dominates the cell and gene therapy pharmaceutical market share by 45%, due to several components that create a strong environment for innovation in biotechnology: an extensive amount of research and development (R&D) funding; an extensive number of nonprofit incubators, world-renowned centers of excellence their associated capabilities; The cell therapy and gene therapy pharmaceutical market in North America leads the rest of the world due to several components that create a strong environment for innovation in biotechnology: an extensive amount of Research and Development (R&D) funding; an extensive number of nonprofit incubators, world-renowned centers of excellence and their associated capabilities; extensive manufacturing capabilities; and supportive Regulatory Agencies who provide clear pathways for companies to confidently take their innovative therapies to market.

Country Level Analysis

The U.S. has many of the major pharmaceutical companies are located within the region, and they continue to work with biotechnology innovators to commercialize their products and accelerate the growth of innovative curative therapies. These factors combine to create a unique and unmatched environment for the development of next-generation medical products in North America.

Why Asia Pacific is Fastest Growing in the Cell and Gene Therapy (CGT) Pharmaceuticals Market?

The Asia Pacific is the fastest-growing cell and gene therapy pharmaceutical market, because of increased investment by healthcare, proliferation of biotech ecosystems and substantial government support for advanced therapies; all of which support the rapid adoption of new technologies driven by demand for personalized medicine in major population centers. Local biotech companies are actively advancing their production capabilities and clinical trials within the cell therapy sector to establish themselves within this competitive landscape, thereby reducing the gap between themselves and their competitors in the West. In addition, regional governments are building the necessary supporting infrastructures, particularly Good Manufacturing Practice (GMP) compliant facilities, to support their self-sufficiency in advanced therapies.

Country Level Analysis

The rapid growth of China is empowered by a supportive government, an abundance of patients and a streamlined commercialization path. Japan remains a strong source of innovation in regenerative medicine and other areas that benefit from a flexible regulatory system that allows faster approvals.

Become a valued research partner with us - https://www.towardshealthcare.com/schedule-meeting

Segment Insights

Therapy Type Segment

Why are cell Therapies dominating the Cell and Gene Therapy (CGT) Pharmaceuticals Market?

The cell therapies are dominating the cell and gene therapy pharmaceuticals market, a transformative intervention for cancers, immune disorders, and regenerative needs. Their ability to modify or replace dysfunctional cells makes them a powerful therapeutic foundation. Hospitals and research centers have gained significant experience with cell handling, pushing adoption even further. Manufacturing networks for autologous and allogeneic platforms are expanding, supporting higher treatment volumes. Clinical success stories continue to boost trust among clinicians and investors. As a result, cell therapies maintain their stronghold as the most established segment in the advanced therapy landscape.

Gene editing and modulation technologies are growing at a breathtaking pace as developers pursue more precise and durable corrections at the DNA and RNA level. The promise of one-time cures for rare genetic diseases is accelerating R&D across multiple pipelines. Toolkits like gene silencers, editors, and modulators are becoming more refined and safer in clinical settings. As delivery methods improve, these therapies are expanding into broader indications beyond rare disorders. Investor enthusiasm is extremely high due to the long-term therapeutic potential. Consequently, gene editing is rapidly becoming the fastest-rising star in the segment.

Modality Segment

Why are Viral Vectors dominating the Cell and Gene Therapy (CGT) Pharmaceuticals Market?

The viral vectors are dominating the cell and gene therapy (CGT) pharmaceuticals market, because of their unparalleled effectiveness in transporting therapeutic genes to the target cells that viral vectors are still the main method. The developers keep using AAV, lentiviral, and other vector types because of their familiar and stable nature, and their good clinical results. The production skills for viral vectors have been greatly elevated, thus making clinical development more efficient. Also, the fact that they can be used in both in vivo and ex vivo therapies, makes them increasingly important. They are still the gold standard for the delivery of genetic payloads, even though they are costly and complicated. Their firm position in the market is what makes viral vectors the main force behind the current success of gene therapy.

Non-viral delivery methods are growing quickly as firms look for less risky, more easily scalable options to viral vectors. Lipid nanoparticles, polymers, and physical delivery devices are becoming more popular because they are more adaptable and less likely to cause immune responses. These carriers make production easier and less dependent on complicated viral supply chains. The possibility of using them for larger or multiple doses is arousing extensive clinical interest. The breakthrough of RNA vaccines has been the main driver of this change. Consequently, non-viral delivery is becoming the leading rapid-growth sector in advanced therapies.

Route of Administration

Why are Intravenous dominating the Cell and Gene Therapy (CGT) Pharmaceuticals Market?

Intravenous administration remains the leading method of treatment because it is the most known, straightforward, and can easily distribute drugs throughout the body. Generally, cellular and animal model gene therapies use IV infusion as a method of delivery. Healthcare providers are highly skilled in IV management; thus the procedure is less complicated. Besides, IV procedures offer the possibility of controlled dosing and monitoring which ensure patient safety. The resources needed for IV therapy are already available in most big hospitals. These points are the reasons why intravenous delivery is the most natural first option for most advanced therapy programs.

Intrathecal administration is rapidly expanding because the developers are focusing on neurological and spinal diseases that need direct access to the central nervous system. This method gets around the blood brain barrier, which makes it perfect for diseases that cannot be treated by systemic methods. Scientists are widely opening trials in rare neuromuscular and neurodegenerative disorders, which is resulting in the rapid development of this field. The clinicians' proficiency is getting higher with the help of specialized techniques as well as better safety protocols. Along with the increase of gene therapies for CNS disorders, intrathecal administration is becoming a strategic priority. Therefore, it is one of the fastest-growing administration routes in the market.

Get the latest insights on life science industry segmentation with our Annual Membership: https://www.towardshealthcare.com/get-an-annual-membership

Manufacturing & Supply Model

Why are n-House Manufacturing by Sponsors dominating the Cell and Gene Therapy (CGT) Pharmaceuticals Market?

In-house production is still the major player because enterprises want to have more control over the quality, timeframes, and the processes that are their proprietary. Precision is what advanced therapies require, and that is what internal facilities can guarantee. Most of the innovators choose to protect the confidentiality of vectors, cell lines, and the tools used in editing. Vertical integration is also a way to lower production costs in the long run, particularly when therapies are scaled. Clinical teams are experiencing an advantage through closer cooperation with the manufacturing units. The combination of control and dependability is the reason why in-house manufacturing is still the prevailing model.

The trend of outsourcing production is picking up speed significantly as the internal capacity cannot meet the demand. CDMOs provide a company with the necessary know-how, offer a flexible work capacity, and can be quickly operational for a company which does not have its own infrastructure. The increase in clinical programs has been a factor that urged developers to seek the help of external partners for viral vector, plasmid, and cell-processing needs. To embrace more talent, CDMOs nowadays are investing more in the construction of modular and multi-modal facilities that are tailored for advanced therapies. Besides, their ability to provide end-to-end solutions, starting from the development phase to fill–finish, is welcoming more customers. Hence, outsourcing the manufacturing process is gradually becoming the dominant model in the ecosystem.

End User Segment

Why are Hospitals & Specialized Infusion Centres by Sponsors dominating the Cell and Gene Therapy (CGT) Pharmaceuticals Market?

Hospitals and specially equipped treatment centers are still the major end users of advanced therapies which mostly demand acute clinical supervision. These centers have the necessary equipment for cell processing, skilled staff, and the ability to monitor. The management of patients undergoing cell and gene therapies is a complicated one, so the dependence on high-tier institutions is increased. Most therapies are given only at certified treatment sites, which thus, fortifies their position. Moreover, their engagement in managing the severest cases further elevates them to be primary users. Such a concentration of experience keeps hospitals at the core of therapy delivery.

As the production is getting decentralized and the development of therapies is becoming increasingly specialized, CDMOs, and contract providers are the group of users whose number is increasing most rapidly. These partners usually take the responsibility for managing analytical testing, process development, and clinical trial supply, if only partly. Relatively to smaller biotechs entering the market, the need for contract partners is growing significantly. Also, through logistics and handling capabilities, CDMOs are broadening their offering of treatment support services. Their participation is instrumental in alleviating bottlenecks and speeding up commercialization timelines. The scope of their involvement is expanding; thus, they are a rapidly rising user segment.

Recent News of Cell and Gene Therapy (CGT) Pharmaceuticals Market:

➜ In August 2025, the U.S. Food and Drug Administration (FDA) granted full approval to PAPZIMEOS (zopapogene imadenovec-drba) for treatment of adults with Recurrent Respiratory Papillomatosis (RRP), a rare disease caused by persistent infection with HPV types 6 or 11.

➜ PAPZIMEOS is the first and only approved therapy for RRP, representing a major milestone for the CGT field because it offers a non-surgical, immunotherapy-based option (four subcutaneous injections over 12 weeks) targeting the root cause (HPV-infected cells) rather than just repeated surgeries.

Value Chain Analysis for Cell and Gene Therapy (CGT) Pharmaceuticals Market

Research & Development (R&D)

Steps:

● Target identification and validation

● Preclinical studies (in vitro and in vivo)

● Development of vectors, gene-editing tools, or cell therapy products

● Process optimization for manufacturing

Key Organizations/Companies:

Novartis, Gilead/Kite Pharma, CRISPR Therapeutics, Sangamon Therapeutics – Gene therapy development, Cellectis,

Academic & research institutions: Harvard Medical School, Stanford University, University of Pennsylvania

Clinical Trials & Regulatory Approvals

Steps:

● Phase I–III clinical trials (safety, efficacy, dose optimization)

● Regulatory submissions to FDA, EMA, PMDA, or other national authorities

● Fast-track or breakthrough designations for accelerated approval

● Post-approval monitoring

Key Organizations/Companies:

Novartis, Bluebird Bio, Sarepta Therapeutics, etc., FDA (USA) – Regulatory oversight, EMA (Europe) – Approval and regulation, PMDA (Japan) – Regulatory review, Contract research organizations (CROs): IQVIA, Parexel, Charles River Labs

Manufacturing & Distribution (optional step for completeness)

Steps:

● In-house or outsourced production (CDMOs)

● Quality control and batch release

● Cold-chain distribution to hospitals and infusion centers

Key Organizations/Companies:

Lonza, WuXi AppTec, Samsung Biologics, Catalent – Contract manufacturing

Patient Support & Services

Steps:

● Patient education and counseling

● Therapy administration support

● Monitoring and follow-up care

● Insurance, reimbursement, and financial assistance programs

Key Organizations/Companies: Novartis Patient Support Programs, Gilead’s KiteCare, Bluebird Bio Patient Services, Hospitals & specialized infusion centers (e.g., Mayo Clinic, MD Anderson Cancer Center)

Top Companies in the Cell and Gene Therapy (CGT) Pharmaceuticals Market

➣ Novartis

➣ Gilead Sciences / Kite Pharma

➣ Bristol Myers Squibb (BMS) / Juno Therapeutics

➣ Roche / Spark Therapeutics

➣ Sarepta Therapeutics

➣ REGENXBIO

➣uniQure

➣ Sangamo Therapeutics

➣ CRISPR Therapeutics

➣ Intellia Therapeutics

➣ Editas Medicine

➣ Beam Therapeutics

➣ Fate Therapeutics

➣ Catalent (Cell & Gene Services)

➣ Lonza (Cell & Gene Solutions)

➣ Thermo Fisher Scientific (including Patheon services)

➣ WuXi AppTec / WuXi Advanced Therapies

Segment Covered

By Therapy Type

● Cell Therapies

○ Autologous Cell Therapies (patient-derived CAR-T, TCR-T, autologous NK)

○ Allogeneic Cell Therapies (off-the-shelf CAR-T, iPSC-derived NK, universal cells)

○ Stem-cell Therapeutics (MSC, iPSC-derived products)

● Gene Therapies

○ In-vivo Gene Therapy (AAV, adenoviral, non-viral delivery)

○ Ex-vivo Gene Therapy (cells modified outside the body then re-infused)

● Gene Editing & Gene Modulation

○ CRISPR/Cas, base editors, prime editors (in-vivo and ex-vivo)

○ Epigenetic regulators, RNA-based modulation (CRISPRa/CRISPRi, antisense oligos)

● RNA & Oligonucleotide-based Therapies

○ mRNA therapeutics for cell engineering or in-vivo expression

○ siRNA / ASO adjuncts to CGT programs

By Modality / Vector & Delivery Platform

● Viral Vectors

○ AAV (Adeno-Associated Virus)

○ Lentivirus / Retrovirus

○ Adenovirus & HSV

● Non-Viral Delivery

○ Lipid nanoparticles (LNPs), polymers, electroporation, nanoparticle platforms for in-vivo and ex-vivo delivery

○ Novel physical delivery (e.g., focused ultrasound, electroporation devices)

● Gene Editing Tools & Platforms

○ CRISPR/Cas families, base/prime editors, meganucleases (often sold as platform tech or licensed)

By Route of Administration

● Intravenous / Systemic Infusion

● Intrathecal / Intracerebral / CNS Direct Delivery (Fastest Growing for CNS programs)

● Intramuscular / Intravitreal / Intratumoral / Localized catheters and implants

By Manufacturing & Supply Model

● In-House Manufacturing by Sponsors

○ Pharma/biotech builds its own suites for the chain-of-identity and control

● Outsourced & CDMO Manufacturing

○ Viral vector CDMOs, cell therapy CDMOs, fill/finish partners, analytical service providers

● Hybrid / Strategic Partnerships

By End User / Customer

● Hospitals & Specialized Infusion Centers

● CDMOs & Contract Labs

● Academic Medical Centers & Clinical Trial Sites

● Specialty Pharmacies & Treatment Networks

By Region

● North America

○ U.S.

○ Canada

● Asia Pacific

○ China

○ Japan

○ India

○ South Korea

○ Thailand

● Europe

○ Germany

○ UK

○ France

○ Italy

○ Spain

○ Sweden

○ Denmark

○ Norway

● Latin America

○ Brazil

○ Mexico

○ Argentina

● Middle East and Africa (MEA)

○ South Africa

○ UAE

○ Saudi Arabia

○ Kuwait

Immediate Delivery Available | Buy This Premium Research @ https://www.towardshealthcare.com/checkout/6099

About Us

Towards Healthcare is a leading global provider of technological solutions, clinical research services, and advanced analytics, with a strong emphasis on life science research. Dedicated to advancing innovation in the life sciences sector, we build strategic partnerships that generate actionable insights and transformative breakthroughs. As a global strategy consulting firm, we empower life science leaders to gain a competitive edge, drive research excellence, and accelerate sustainable growth.

You can place an order or ask any questions, please feel free to contact us at sales@towardshealthcare.com

Europe Region: +44 778 256 0738

North America Region: +1 8044 4193 44

APAC Region: +91 9356 9282 04

Web: https://www.towardshealthcare.com

Find us on social platforms: LinkedIn | Twitter | Instagram | Medium | Pinterest